Purpose of this article: to explain what goes into your credit score and give you tips to improve your overall credit score.

Overview

Your credit score is a number that approximates how likely you are to repay your debt. This number is used by lenders to decide whether or not to approve you for new loans. And while your overall credit history is captured and maintained by the three main credit bureaus (Equifax, Experian, and TransUnion), the actual score is calculated by the VantageScore and FICO models.

Credit scores range from 300-850 and your score within this range is based on many factors such as how often you make payments on time, and how many accounts you have in “good-standing.”

It is possible at any given time to have different scores given the various scoring models that are in place, but the bottom line is that your score is based on the information within your credit report. It’s a good habit to review this information annually to ensure that it is correct. You can access your free annual credit reports from here.

The Main Factors that Affect Your Score

The factors that are generally considered when calculating your credit score are as follows:

• Payment history – do you pay your bills on time every time?

• Length of credit – how long have you had your accounts open?

• Type of credit – are your loans auto, student, mortgage, credit cards, etc.

• Use of credit limits – how much of your available credit limits is currently used up?

• Number of hard inquiries on your credit report

Why Does Your Credit Score Matter?

Since credit is simply borrowed money provided in the form of a loan, credit issuers like banks or other financial institutions want to make sure of your likelihood to repay. Consequently, they use your credit score as this indicator. Low scores indicate lower degree of repayment while higher scores indicate a higher degree of paying on time.

The amount of money you can borrow as well as the interest that you will be charged is primarily determined by your credit score rating and where you fall in the range. This is why your credit score really matters!

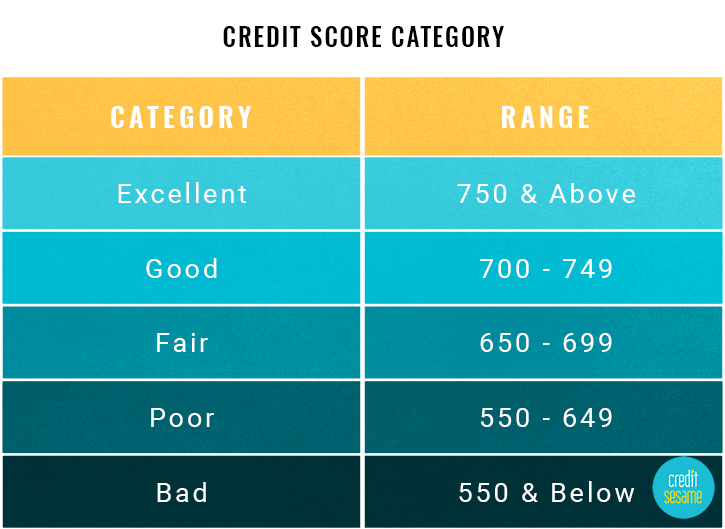

The following score range comes from Credit Sesame:

{kind=link}

You don’t necessarily need perfect credit to get the best interest rates and borrowing options, but the closer you are to the 700+ range the better off you will be.

The Formula to Getting a Better Score

Given everything we have talked about the formula to getting a better credit score is pretty simple:

1. Payment History (35%)

Pay all of your bills on time… no exceptions!

2. Credit Utilization (30%)

Do not use more than 30% of your available credit at any given time. If you are above 30% today, call up your credit card companies and ask them to increase your available credit. Doing so can instantly drop your utilization rate!

3. Age of Credit (15%)

Hold off on closing down old accounts because longer credit history is beneficial to your credit score

4. Type of Credit Outstanding (10%)

Mix the type of loans you have. Credit card debt (i.e. revolving credit lines) are penalized more than mortgage, auto, personal, and or student loans. Put another way, debt that is usually not tied to an asset is penalized more from a credit score standpoint.

5. Number of Hard Inquiries (10%)

Don’t open more than 2 credit cards a year. Usually new credit cards require a hard inquiry into your credit history and that negatively impacts your credit score

*Please note that this breakdown is based on the FICO scoring system. The VantageScore 3.0 credit scoring system weight each variable slightly different but Payment History is still the most important under both scoring systems.

Closing

Your credit score is one of the most important three-digit numbers you will manage in your financial life. It really can mean the difference between thousands of dollars paid over the life of a loan. When it comes to maximizing your credit score, the steps detailed within this article are the easiest and most effective ways to do so. If you only do two things, please make sure you pay your bills on time and call your credit card company today to ask for more available credit. My hope in writing this article is that after reading this, you will take some steps towards improving your credit score.

On an aside: If you currently do not use a credit monitoring service, please sign up for Credit Karma as soon as possible. It’s free to use, very effective, and can help protect you from fraudulent activity on your credit reports. Given the Equifax hack that occurred earlier this year, it’s imperative that we all monitor our credit more closely these days.