"Let everyone else call your idea crazy ... just keep going. Don't stop. Don't even think about stopping until you get there, and don't give much thought to where "there" is. Whatever comes, just don't stop."

--- Phil Knight, Shoe Dog (2016)

Introduction

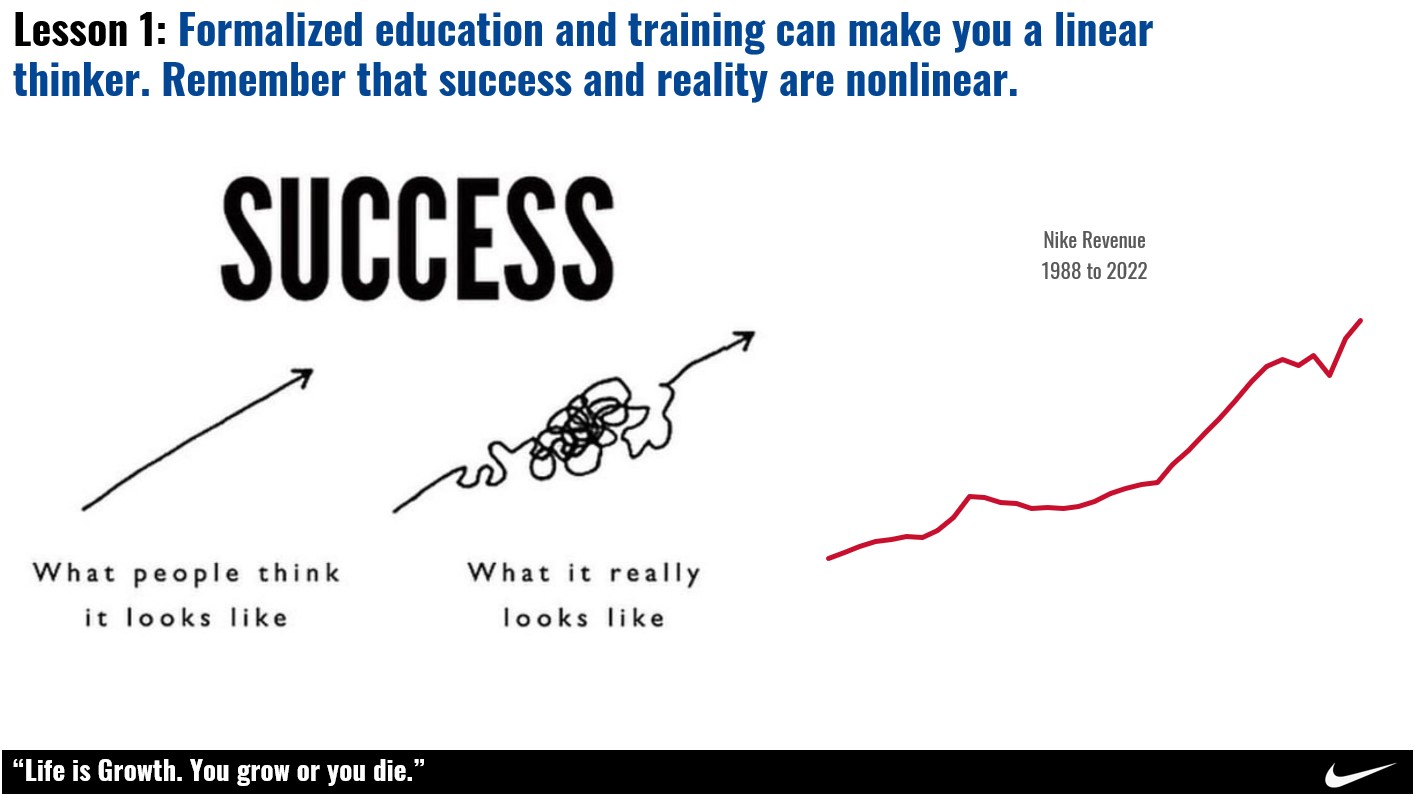

In 1965, Phil Knight discovered a philosophy by which he centered everything he was doing: To have cash balances sitting around doing nothing made no sense to me. Sure, it would have been the cautious, conservative, prudent thing. But the roadside was littered with cautious, conservative, prudent entrepreneurs. I wanted to keep my foot pressed hard on the gas pedal.

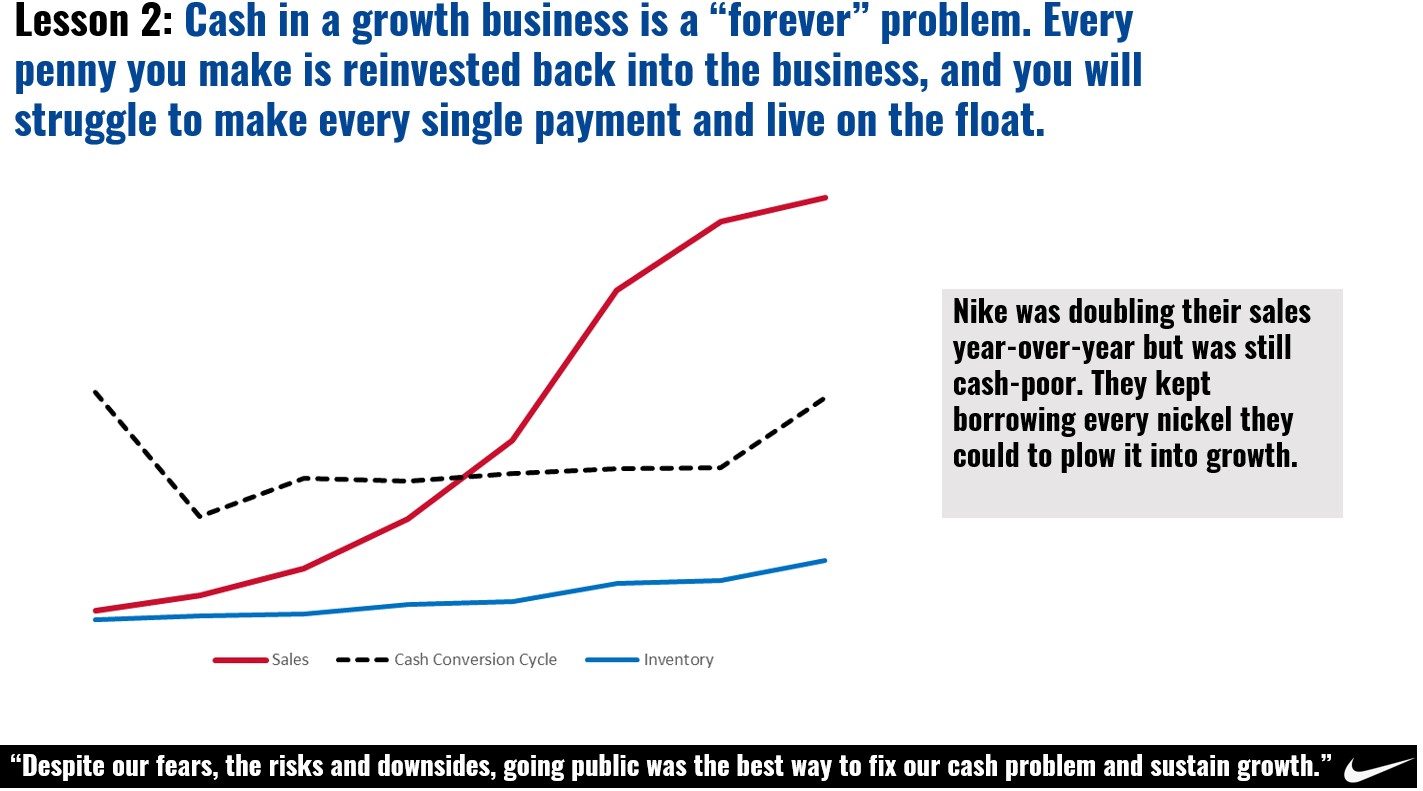

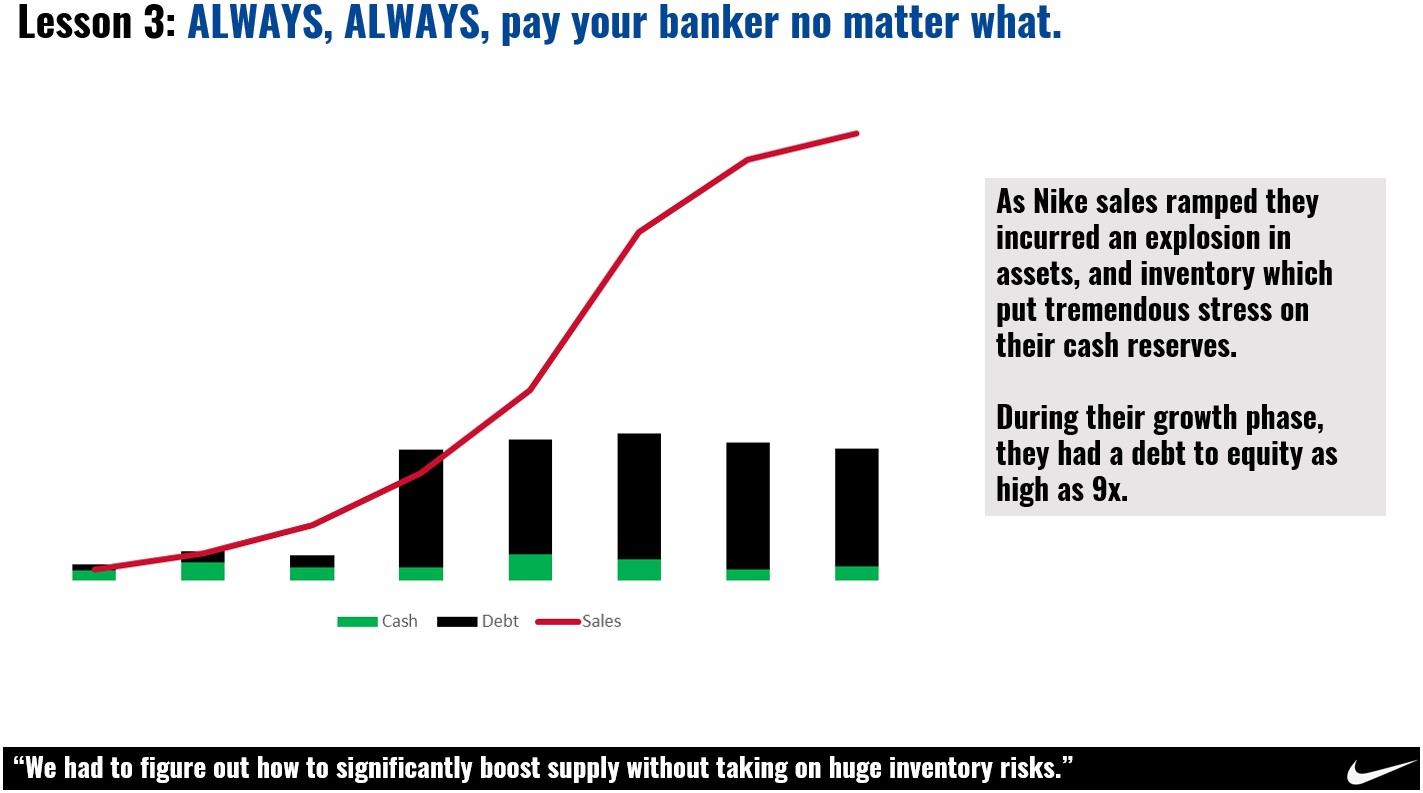

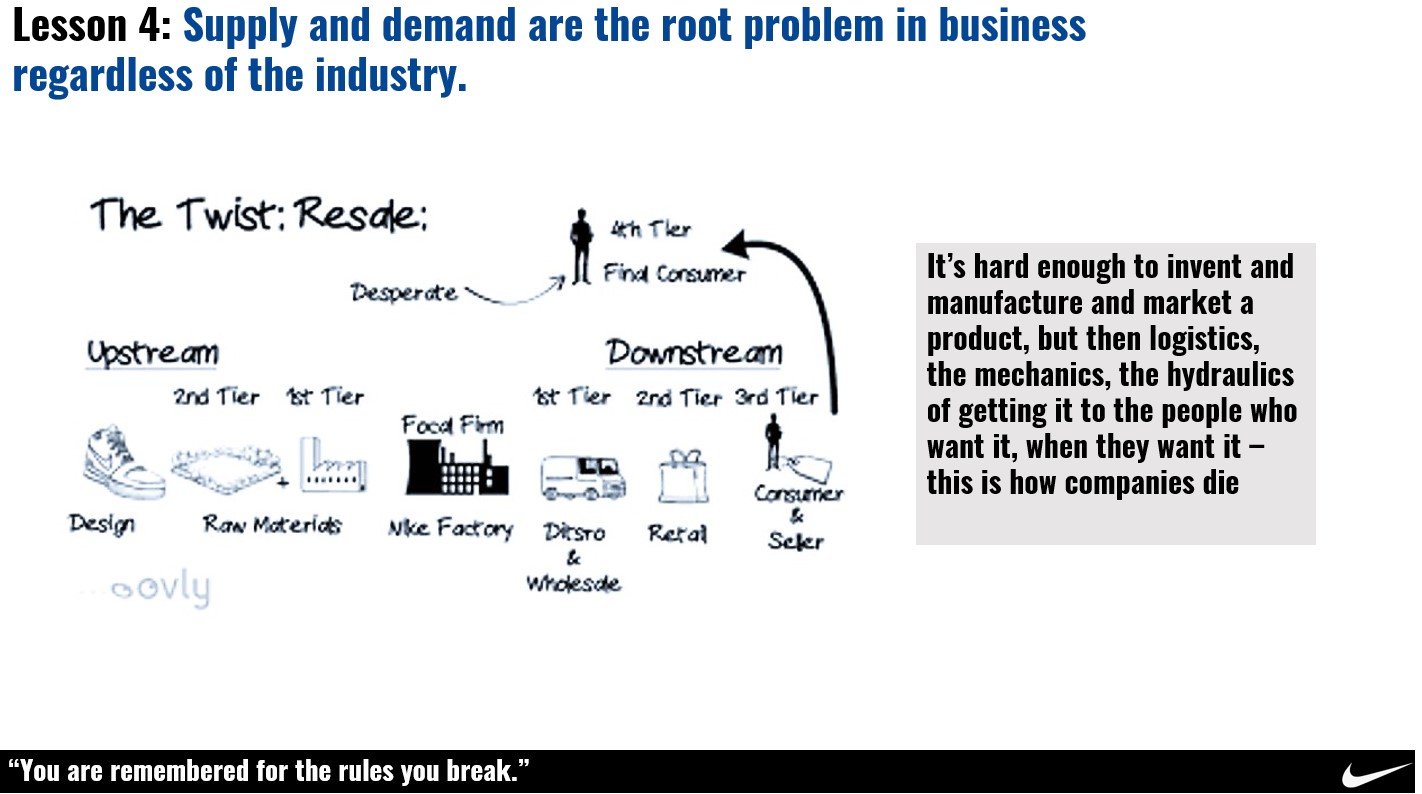

By 1975, he was still having the same problem as they were undergoing an explosion in assets and inventory which continued to put enormous strains on their cash reserves. Sales were through the roof but they were still cash-poor. Fast forward to today, and Nike is a cash-rich business whose days of cash constraints are long gone!

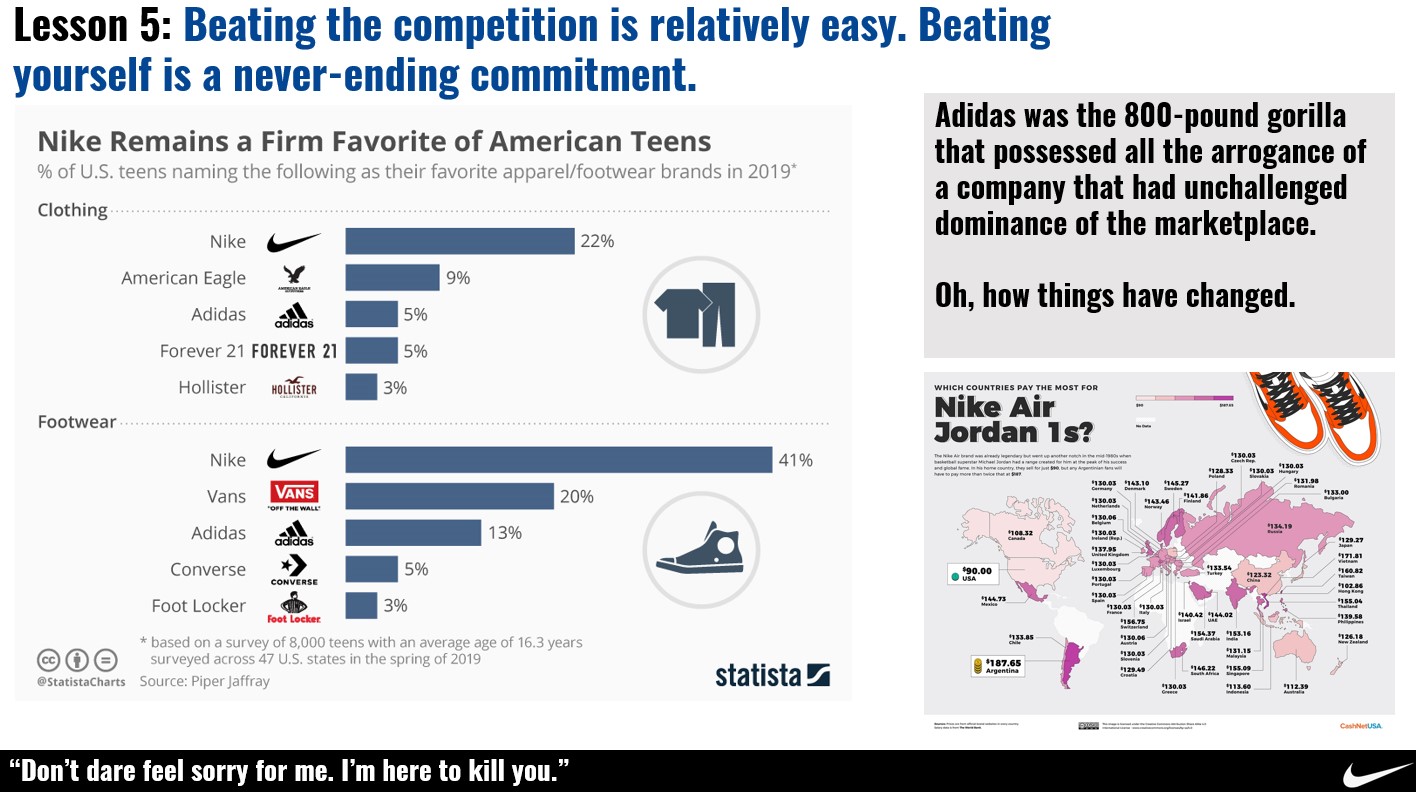

The lesson I take away from reading this memoir is that cash in a growth company is a problem. Every penny you make will be reinvested back in the business and you will struggle to make every single payment. You will borrow every nickel you can and plow it right back into chasing growth. But always remember that fortune favors the brave. Beating the competition is relatively easy. Beating yourself is a never-ending commitment.

"The Smart Machine Age will usher in an era where the smartest humans are not those that have the deepest knowledge"

--- Edward Hess & Katherine Ludwig, Humility is the New Smart (2017)

Summary

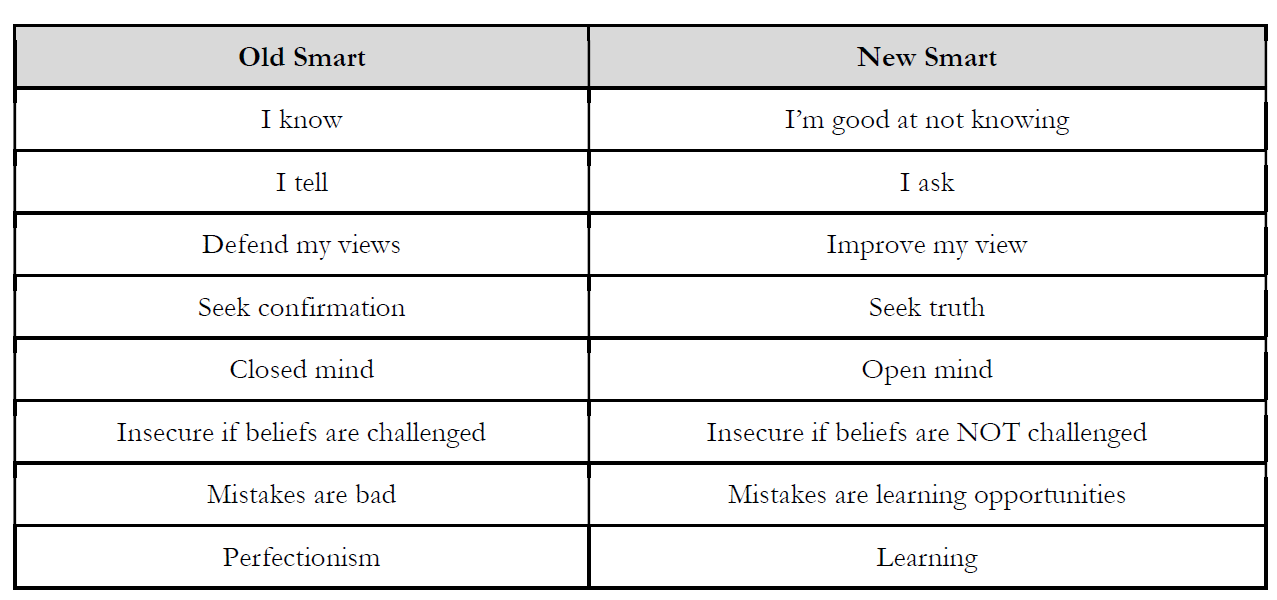

With the dawn of the Smart Machine Age, humans need a new playbook to thrive. That playbook is laid out in detail by Edward Hess and Katherine Ludwig in Humility is the New Smart. In order to reach “New Smart” you need to:

(1) Quiet your ego

(2) Manage yourself (emotions & thinking)

(3) Reflectively listen

(4) Emotionally connect & relate to others (otherness).

This section contains PowerPoint “art”, sketches, visual summaries, and “flashes of insights” for use in presentations and more. If you like any of the content posted on this page, consider supporting my efforts with a cup of coffee or a donut ☕?.

Life is Non-Linear by Brian NwokediGrowth Businesses Never Have Enough Cash by Brian NwokediAlways Service Your Debt by Brian NwokediCompetition is Yourself by Brian NwokediCompetition is Yourself by Brian Nwokedi

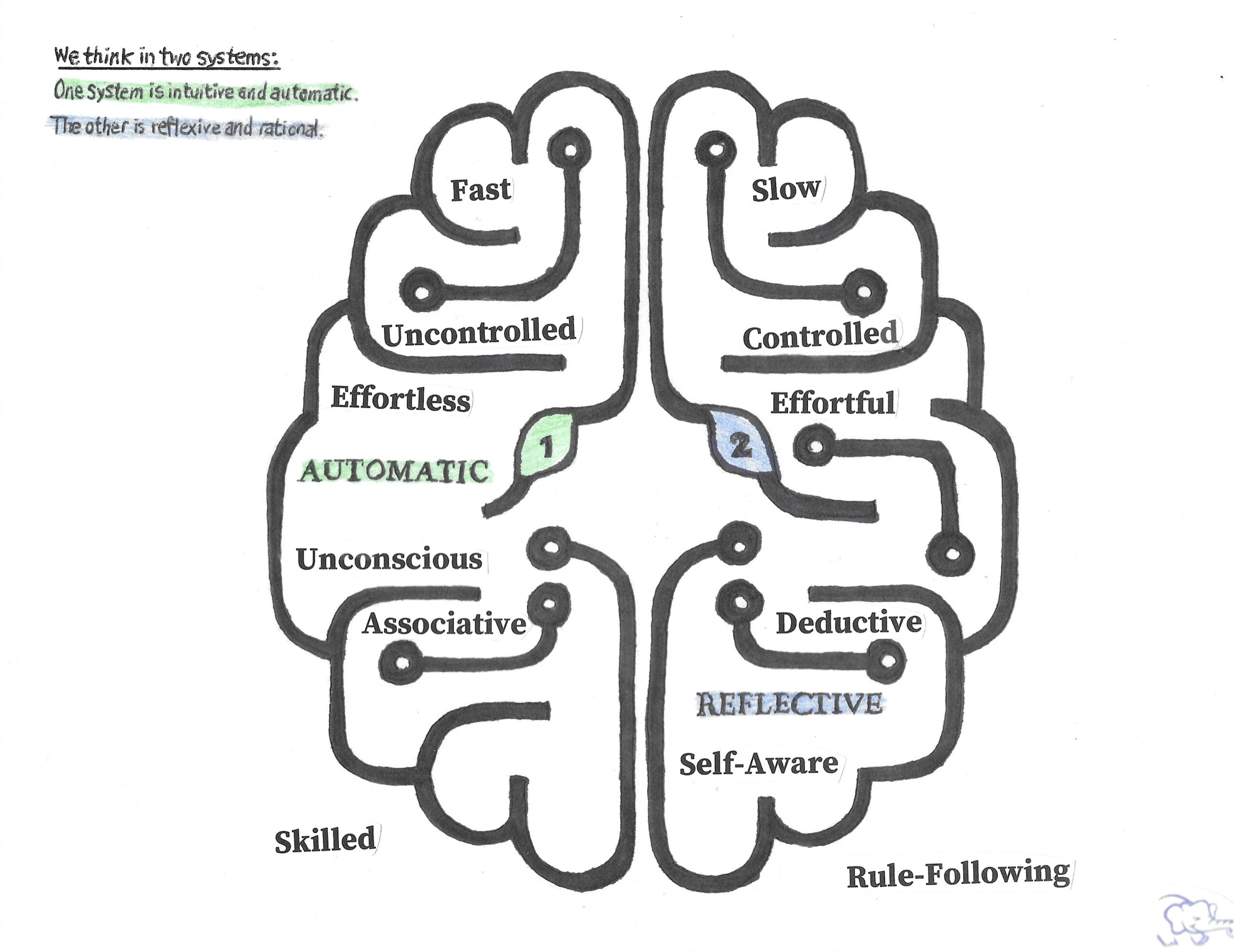

Thinking Fast and Slow Picture Summary by Brian Nwokedi. There are two systems of thought: The Intuitive System 1 and the Effortful System 2

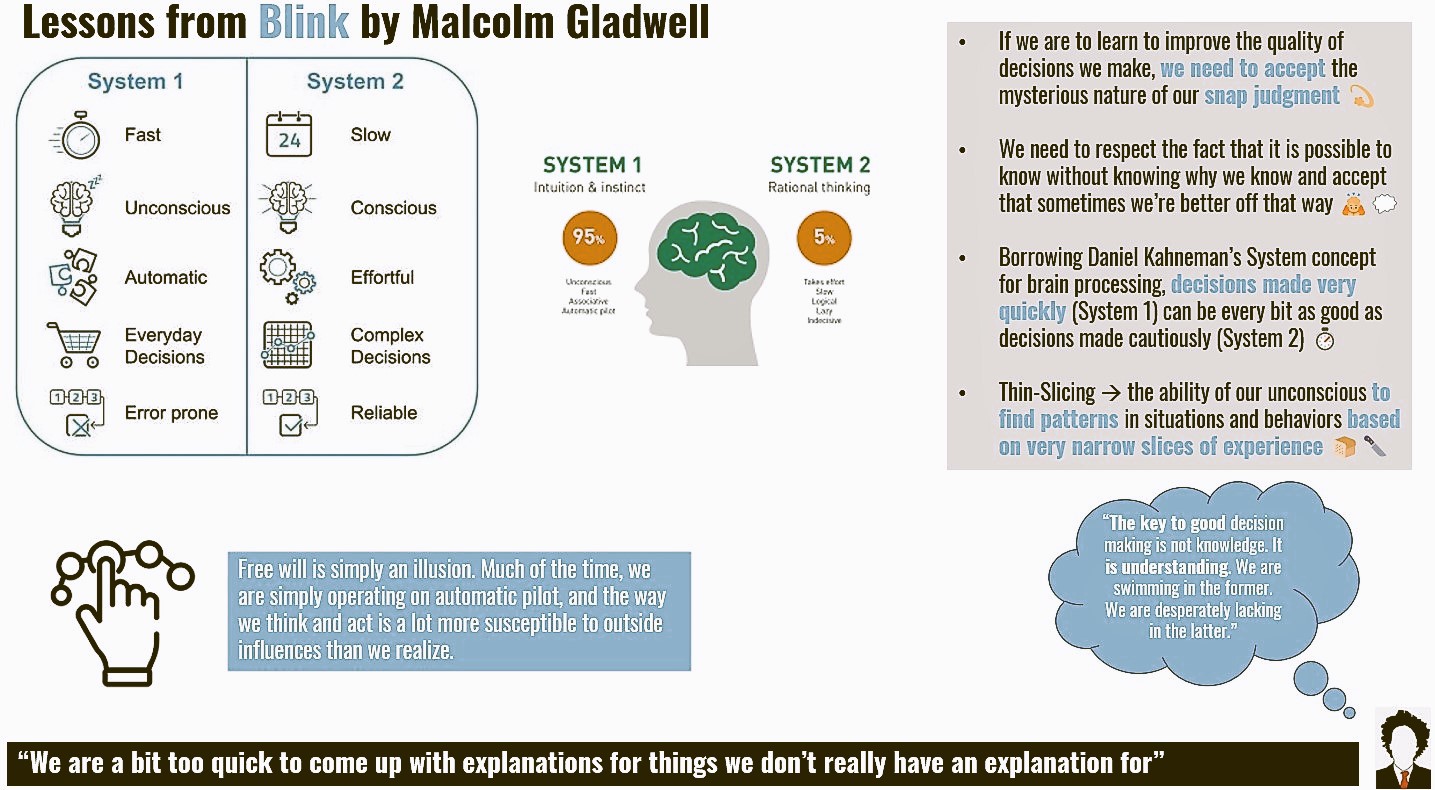

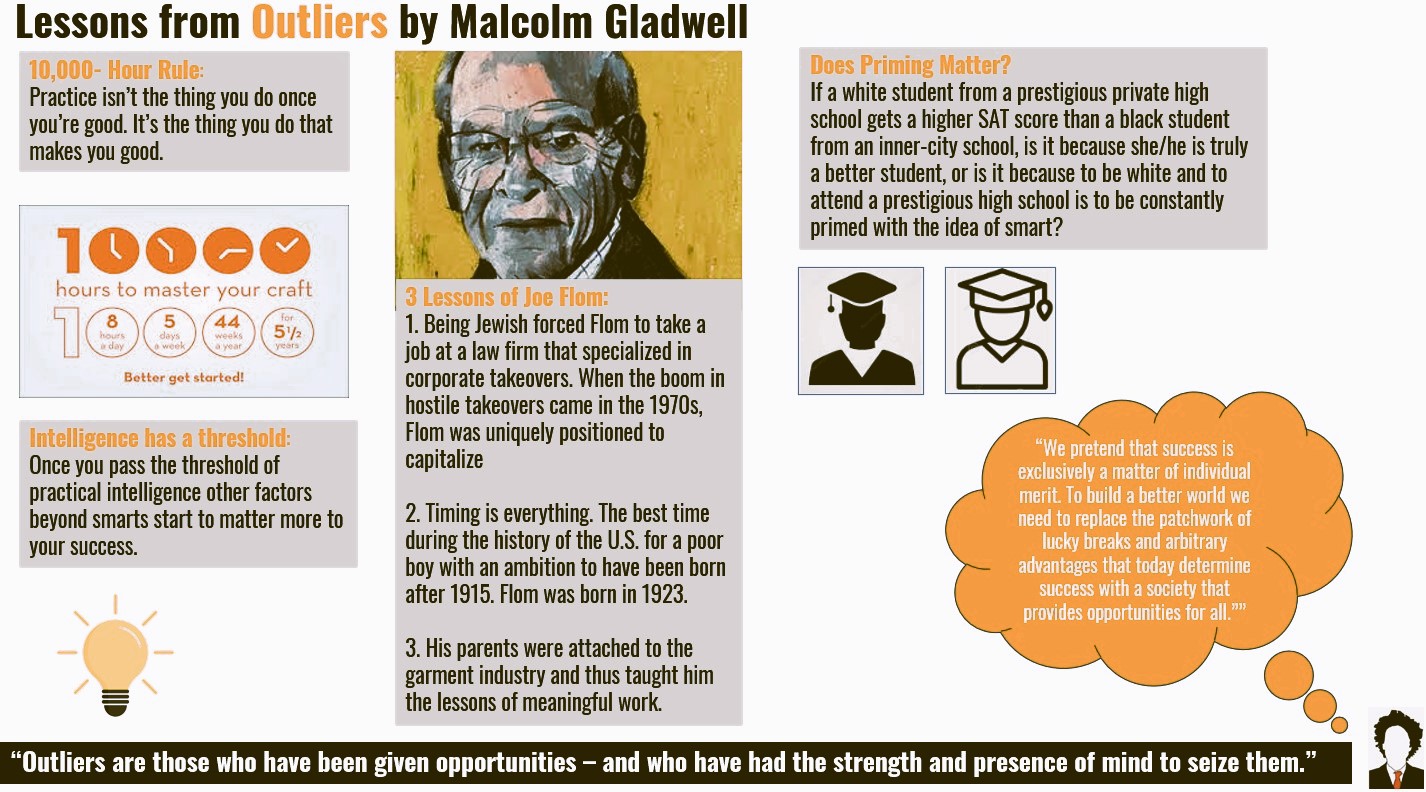

Wisdom of Malcolm Gladwell:

If we are to learn to improve the quality of decisions we make, we need to accept the mysterious nature of our snap judgments. We need to respect the fact that it is possible to know without knowing why we know and get that sometimes we’re better off that way.Outliers are those who have been given opportunities – and who have had the strength and presence of mind to seize them. To build a better world we need to replace the patchwork of lucky breaks and arbitrary advantages that today determine success – the fortunate birth dates and the happy accidents of history – with a society that provides opportunities for all.

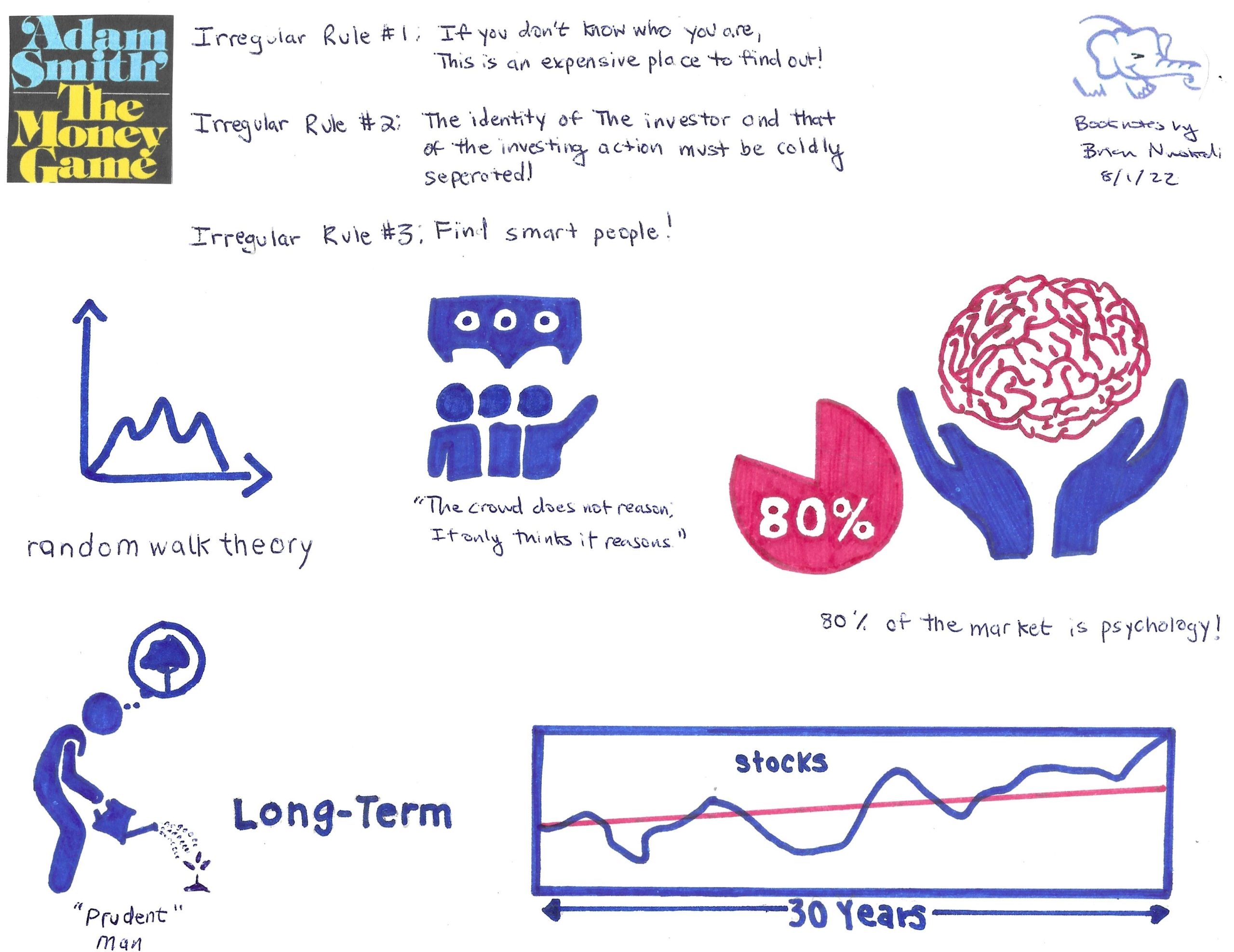

What if I told you that the whole point of the stock market is not to make money? What if I told you that the stock market itself is just a Game, and the real object of this Game is not money; it’s the playing of the Game itself?

In The Money Game Adam Smith (also known as George J. W. Goodman) sets out to explain how the stock market is a Game to be played with objectives that oftentimes do not make sense. While money preoccupies so much of our consciousness, The Money Game is adamant that making money is not the real objective of playing the stock market Game. The sooner we realize that the stock market Game is an irrational one, the better we will play it.

Through a series of chapters asking questions and describing real events and real characters (real but masked), George J. W. Goodman sets out to explore the unexplored area of the markets … the emotional area. As he states very eloquently in Chapter 2, “There are fundamentals in the marketplace, but the unexplored area is the emotional area. All charts and breadth indicators and technical palaver are the statistician’s attempts to describe an emotional state.

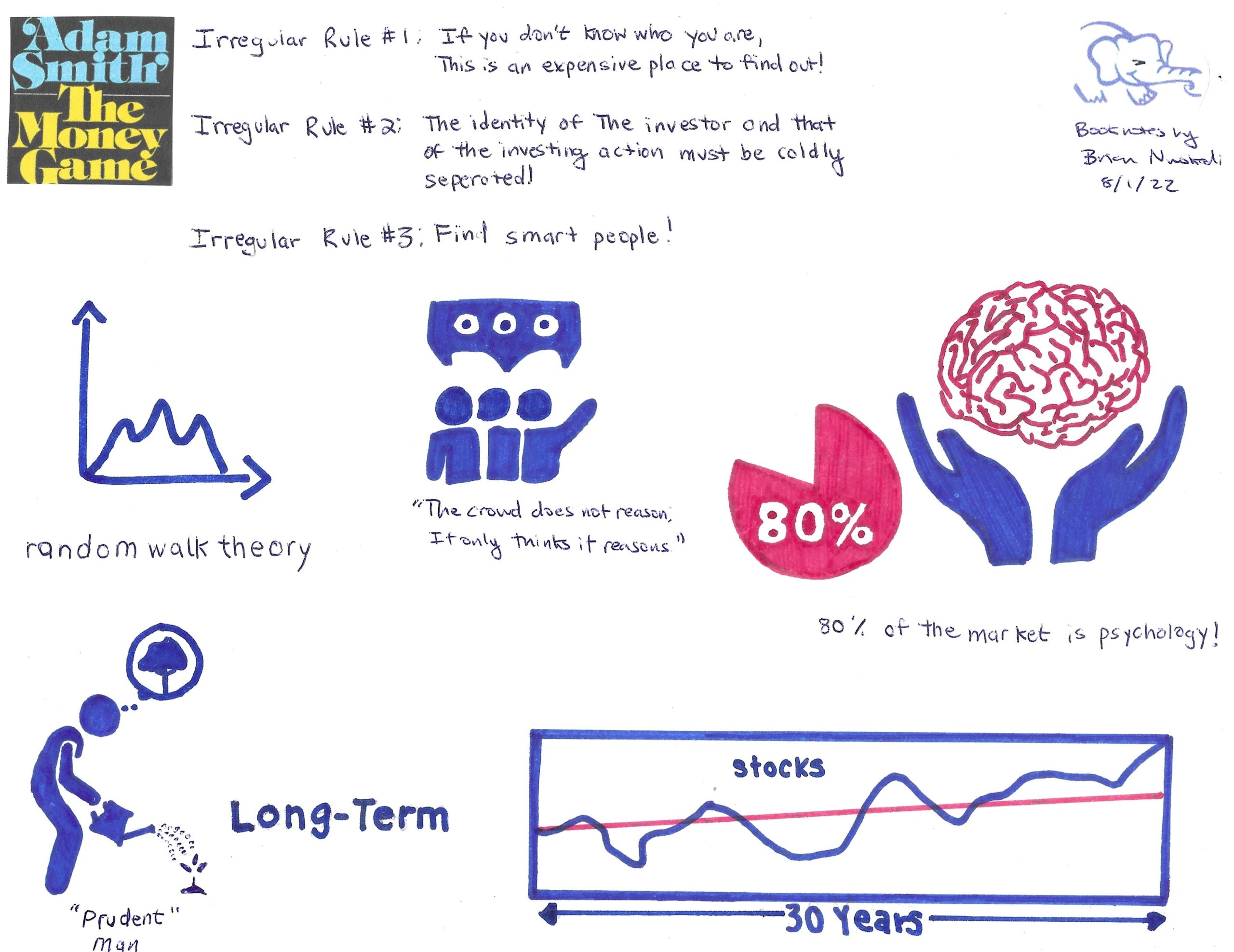

In the end, the one requirement to win The Money Game is to remember the Irregular Rule: If you don’t know who you are, this is an expensive place to find out. Emotional maturity must be displayed over the long run if you are going to survive the game called the stock market.

My Summary Conclusions from Each Chapter

Part I. YOU: Identity, Anxiety, Money: Chapter 1-9

Preface: The game we create with it is an irrational one, and we play it better when we realize that, even as we try to bring rationality to it.

• Chapter 1: The word game was deliberately chosen to describe the stock market and the sooner that all of us small investors understand that this is a game, the better off we may be.

• Chapter 2: Do not forget the Irregular Rule: If you don’t know who you are, this is an expensive place to find out!

• Chapter 3: It all comes back to the Irregular Rule that you must know yourself for the stock market is an expensive place to find that out. The requirement to win this game is emotional maturity.

• Chapter 4: Since 80% of the market is psychology or deeper still human emotionality, the market can really be seen as a crowd. Because of this tendency, there is no substitute for good information, good research, and good ideas.

• Chapter 5: On one hand you have Adam Smith the father of modern economics stating definitely that money is about the maximization of profit and in some sense the accumulation of wealth (i,e. The Wealth of Nations). On the other hand, you have Norman Brown who sees money as a noose around our necks that ultimately makes our human nature impoverished. You must decide for yourself!

• Chapter 6: There are countless reasons people get into the Game. Some people love to gamble and lose. Others just want to make money over the long term by owning stocks forever. Regardless of your reason, you need to know yourself and stick to your plans.

• Chapter 7: The only real protection against all the ups and downs of the market (the anxiety) is to have an identity so firm it is not influenced by all the brouhaha in the marketplace. And remember, the stock doesn’t know you own it!

• Chapter 8: So if we are talking about real big money, forget the stock market. Build a company and have the market capitalize on your earnings.

• Chapter 9: The “simple equation of wealth”: To get rich, you find a stock whose _ has been compounding at a very fat, and then the stock zooms, and there you are.

Part II. IT: Systems: Chapter 10-14

Chapter 10: Charting assumes that what was true yesterday will also be true tomorrow. But you and I know that past patterns/performance are not predictive of future patterns/performance.

• Chapter 11: To quote Professor Fama, “the history of the series of stock price changes cannot be used to predict the future in any meaningful way. The future path of the price level of security is no more predictable than the path of a series of cumulated random numbers. If the random walk is indeed Truth, then all charts and most investment advice have the value of zero, and that is going to affect the rules of the Game.

• Chapter 12: The Game is such that computers take away any long-term advantages individuals find. Our only chance is to rely on luck (random walk thesis).

• Chapter 13: The numbers created by “independent auditors” should be looked at with a grain of salt given that the accountants are paid and hired by the companies themselves.

• Chapter 14: Someone has to be on the losing end of the transaction and that is usually the little investor.

Part III. THEY: The Pros: Chapter 15-18

Chapter 15: Professional investors are “performance” managers who are focused on driving results in the short term. Very few “performance” managers think in the long term. It’s all about driving big capital gains!

• Chapter 16: Like everything in life, those that are really in the know!

• Chapter 17: The market does not follow logic, it follows some mysterious tide of mass psychology.

• Chapter 18: If you are in the right thing at the wrong time, you may be right but have a long wait; at least you are better off than coming late to the party.

Part IV. VISIONS OF THE APOCALYPSE: Can it All Come Tumbling Down? Chapter 19-20

Chapter 19: Sooner or later you have to come to reality, and stop being a father to the world. Lead it, yes. Buy it. No.

• Chapter 20: Sure, it can all come tumbling down. All it takes is for belief to go away!

Part V. VISIONS OF THE MILLENNIUM: Do You Really Want to Be Rich?

Chapter 21: You need to create your own money philosophy to answer the question do you really want to be rich?

Visual Summary of Key Findings from Book

“Unfortunately, as we have seen, the playing of the Game is not entirely a rational affair. There is nothing so disastrous, said Lord Keynes as a rational investment policy in an irrational world”

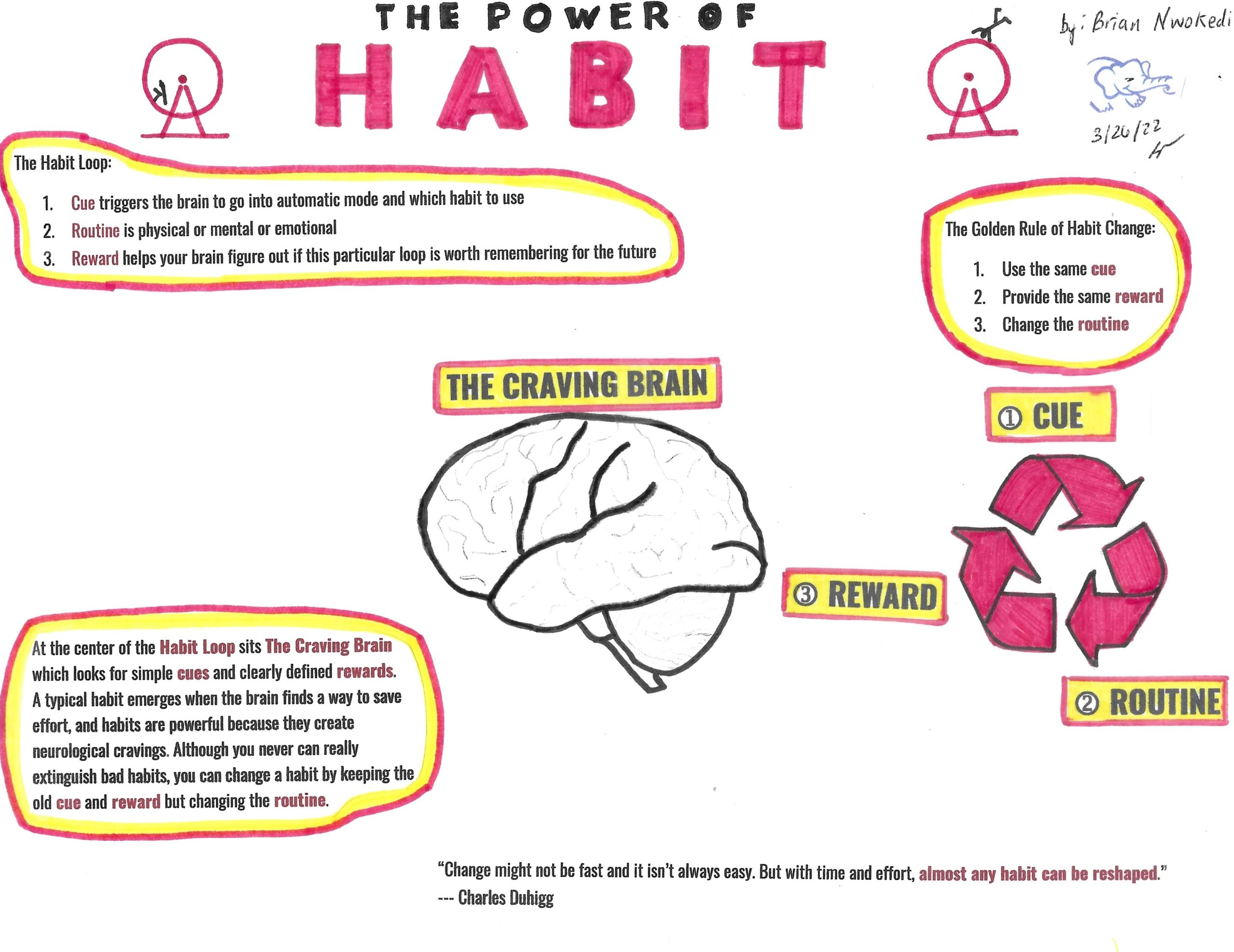

"Change might not be fast and it isn't always easy. But with time and effort, almost any habit can be reshaped."

--- Charles Duhigg, The Power of Habit (2012)

Summary

At the center of the Habit Loop sits the Craving Brain which looks for simple cues and clearly defined rewards. A typical habit emerges when the brain finds a way to save effort, and habits are powerful because they create neurological cravings. When a habit emerges, the brain stops fully participating in decision-making. Although you never can really extinguish bad habits, you can change a habit by keeping the old cue and reward but changing the routine.

Three-Step Loop

A cue triggers the brain to go into automatic mode and which habit to use

The routine is physical or mental or emotional

The reward helps your brain figure out if this particular loop is worth remembering for the future

How To Change a Habit

By focusing on the keystone habit, you can fix a myriad of other habits in the process. You must work to identify cues and choose new routines in order to change your habits. But for habits to permanently change, people must believe that change is feasible.

In closing, to modify a habit, you must decide to change it. You must consciously accept the hard work of identifying the cues and rewards that drive the habits’ routines and find alternatives. You must know you have control and be self-conscious enough to use it.

The real power of habit is the insight that your habits are what you choose them to be. It is important to note that no matter how strong our willpower is, we are guaranteed to fall back into our old ways once in a while

"Iowa State's upward rise has been all about identifying and developing talent"

--- Blair Angulo & Steve Wiltfong of 247 Sports

The foundation is built for Iowa State Football heading into the 2022 season. Although they lose a lot of veteran starters like Brock Purdy and Charlie Kolar, recruiting has picked up substantially. Iowa State is slowly becoming a solid contender for the Big 12 year in and year out.

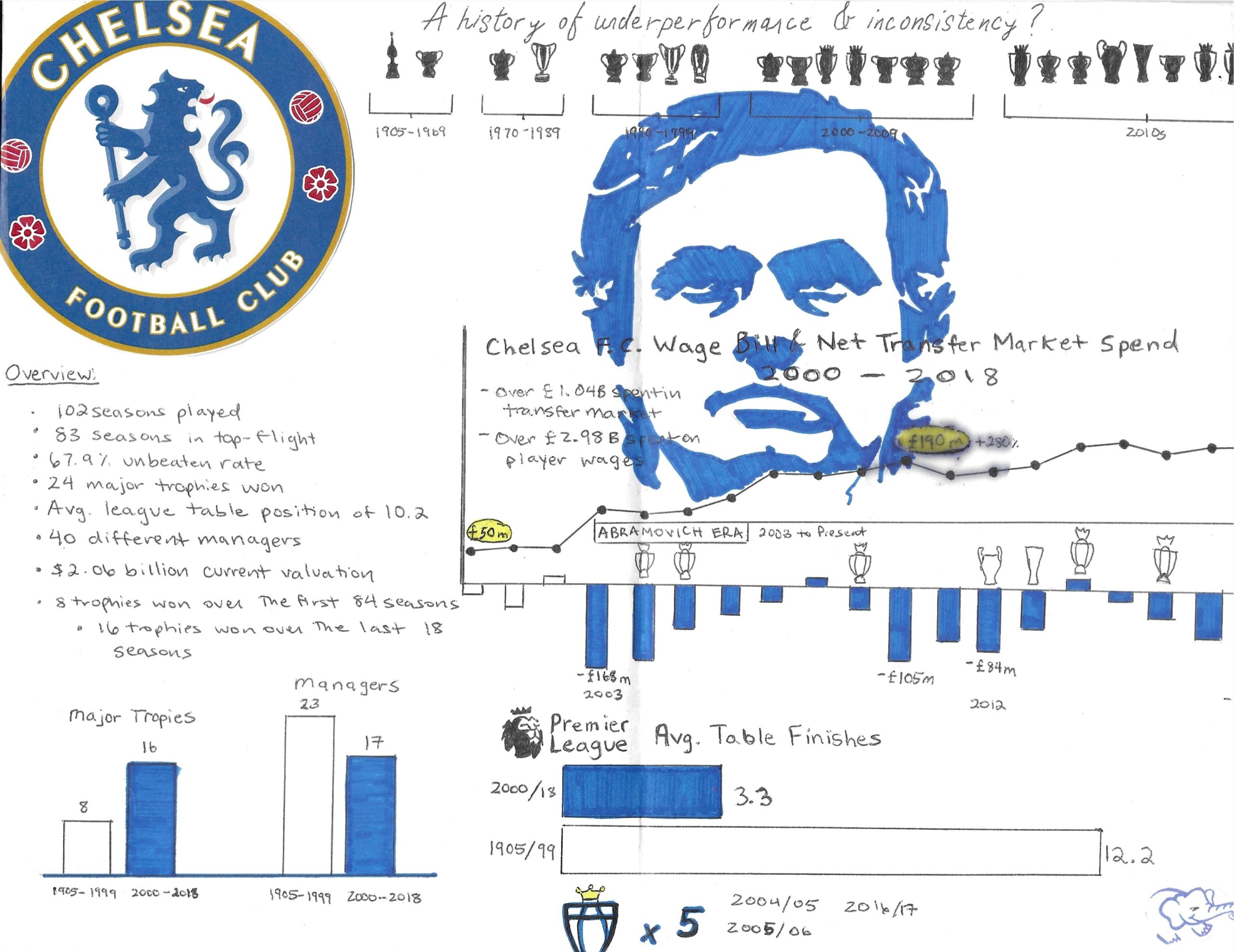

"I would like to address the speculation in media over the past few days in relation to my ownership of Chelsea FC. As I have stated before, I have always taken decisions with the Club’s best interest at heart. In the current situation, I have therefore taken the decision to sell the Club, as I believe this is in the best interest of the Club, the fans, the employees, as well as the Club’s sponsors and partners."

--- Roman Abramovich. March 3, 2022

Chelsea FC has averaged winning one major trophy a year since Roman Abramovich took over in 2003. They are also only 1 of 5 teams in Europe to win every single major trophy at least once.

“The ability to make good decisions regarding people represents one of the last reliable sources of competitive advantage, since very few organizations are very good at it.”

Most companies would agree that the single most important driver of organizational performance and individual managerial success is human capital or talent. Yet most companies still leave their talent acquisition process to chance using outdated interview techniques that lead to poor long-term results.

In June of last year, I read Topgrading by Bradford D. Smart as I geared up to hire a Director of HR. And like “every important business book” out there, Topgrading has been recommended by every who’s who in the business world. I honestly must say that the book is chalked full of strategies that promise to improve your talent acquisition process. I could spend 30+ days trying to unpack all the different tidbits I obtained by finishing this read, but I won’t. Instead, I want to share how my approach to talent acquisition has changed as a result of reading this book.

The Current Reality

The cold reality is that the average company suffers a 75% failure rate hiring people. 75% of managers hired externally without Topgrading methods are mistakes, underperformers, or miss-hires. The following chart shows the reality of talent dispersion:

The Goal

The directly stated goal of Topgrading is to fill at least 75% of positions in an organization with high performers (A Players) by hiring and promoting people who turn out to be high performers at least 75% of the time.

Topgrading companies, in contrast to their competitors, get disproportionately better talent for the total compensation dollars they spend. As ruthless as it may sound, Topgrading is all about increasing the percentage of high performers, A Players, and not being satisfied with B Players who never are worthy of a Very Good or Excellent rating.

The How and What

When you finish reading Topgrading, you are introduced to the Topgrading Interview process where you spend close to a full day accessing your potential hire. You take a chronological approach starting with school years and progressing through many questions about every job starting with the first job and moving forward to the present. The proven magic of Topgrading interviewing is to learn how the candidate has evolved across the education years and full career history.

During this tenacious interview process, you will spend hours accessing 50 separate competencies across five domains:

Intellectual

Personal

Interpersonal

Management

Leadership

The following chart details the 50 competencies and ranks each competency across three dimensions of people’s ability to change their behaviors related to each competency.

50 Specific Competencies For Managers

Most companies have 5 to 10 competencies for most jobs, but the Topgrading method believes that for management jobs these 50 competencies are all important. This means that if a new hire is only Fair or Poor on even one of the above competencies, that new hire is apt to be considered a miss-hire. How tenacious is that?

Resourcefulness is the Most Important Competency

Early in the book (Smart, 2005, p. 36), Bradford D. Smart unequivocally states that resourcefulness is the most important competency to hire for. Resourcefulness (Initiative) is defined as:

“Passionately finding ways over, around, or through barriers to success. Working to achieve results despite lack of resources. A willingness to go beyond the call of duty and a bias for action. A results-oriented “doer.”

Resourcefulness is a composite of several competencies. It’s proactivity, energy, passion, analytical skills, and persistence wrapped into one. In common terms, resourcefulness is the brains and drive to figure out how to get over, around, or through barriers to success. A Players all exude resourcefulness in spades. C Players never seem to develop it.

Resourcefulness is a crucial leadership skill for today’s generation of leaders. A resourceful person is one that is able to quickly adapt to new or different situations, is able to find solutions, think creatively, and sometimes manage with what they have available to them. Given today’s challenges leading during the COVID-19 pandemic, everyone is having to learn how to make do with what they have and develop a skill in doing more with less (Hardwick-Smith, 2020).

A Players Do The Following Really Well…

What I Will Do Differently

As a knowledge-work leader, the key to my success, in the simplest terms, is to hire the best employees, create an empowering environment, provide the necessary tools and guidance, and then get out of the way. I must continuously align individuals’ responsibilities to be consistent with their strengths, weaknesses, and interests.

“At the end of the day, you bet on people, no strategies”

—Larry Bossidy

As a result of finishing this book, I will do some things differently in my talent acquisition approach. Specifically:

I will look harder to find talent at all salary ranges. The focus will be on hiring A Players at the right salary level. Regardless of what we pay people, we should be sure to get top talent for the salary we can afford.

I will screen harder on the front end to select the right people. Time is a precious resource but more time needs to be spent in the phone screening process to eliminate B and C Players upfront.

I will act more quickly to confront nonperformance and redeploy chronic B and C Players.

I will use 360 email surveys and skip-level meetings to gain deeper insights into every manager’s strengths and weaker points, including myself!

In closing, the name of the game is to create talented teams that drive towards better results over the long term. As Peter Drucker so eloquently put it, “Culture eats strategy for breakfast & lunch.” Topgrading will help me prevent the 75% failure rate in hiring and promotions that are so commonplace in most companies. But almost more importantly, it will help me solve the three biggest hiring problems:

Rampant dishonesty by weak candidates who easily get away with fudging their resumes and faking their interviews,

Insufficient information, because most companies use superficial hiring methods that enable candidates to control and hide what they share about themselves,

Lack of verifiability, as most reference checks are practically useless.

An integrated brain is the foundation of resilience and well-adjusted children. The Whole-Brain Child by Daniel J. Sigel and Tina Payne Bryson breaks down 12 simple and easy-to-master strategies that will help you respond more effectively to difficult situations with your child, and build a foundation for strong social, emotional and mental health.

You should read this book to better understand how to turn the everyday “survival” moments as parents into thrive moments, where the important and meaningful work and connecting of parenting can take place.

Never forget that we parents can provide the kinds of experiences for our children that will help them develop a resilient and well-integrated brain!

Having finished the 750+ page tome to Capital by Thomas Piketty well over a year ago, I have just gotten around to writing up what I learned. In attempting to summarize this book, I realize that there is no way I can cover everything I learned. Quite simply, Piketty has blown my mind with the depths of his research. This book is the deepest source I have ever read on how capital behaves and why wealth and income inequality are two sides of different coins.

I figure that the best approach with this write-up is to break it down into manageable chunks. What follows below is a summary of the theoretical characteristics of Capital and how it behaves in the world today as well as in the past. I’ll unpack the features of income, capital, and output and how each of these dynamics interplay with one another.

The next write-up at a later date yet to be determined, will delve into the impacts that Capital has had on inequality. I’ll unpack the structure of inequality and some potential solutions that Piketty mentions. This review is by no means a political or opinion piece. I am simply sharing some of the learnings I received from diving into this book.

With that, let’s dive in…

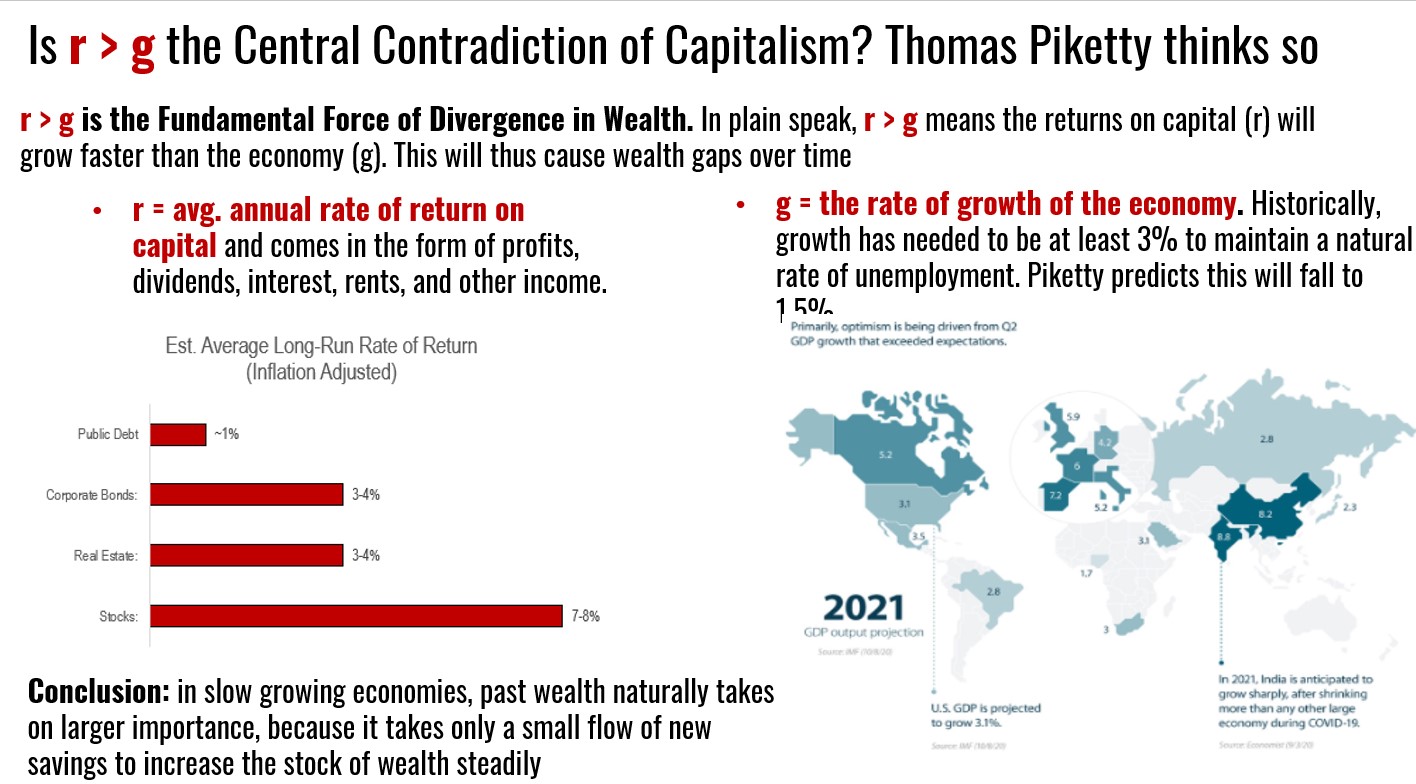

Is r > g the Central Contradiction of Capitalism?

The first concept that Piketty spends time unpacking is the relationship between returns on capital and the overall growth rate of the economy. Piketty boldly states that growth in the future will slow and capital will be that much more important. As economic growth slows and falls below the average rate of return on capital, past wealth naturally takes on a larger importance. This is simply because it takes only a small flow of new savings to increase the stock of wealth steadily.

Thomas Piketty’s First Fundamental Law of Capitalism

The second concept that Piketty spends time unpacking is what he calls his First Fundamental Law of Capitalism. This law shows how important capital is in relation to the national income of a country. As the nature of wealth over the long run continues to transform (i.e., capital used to be agricultural and has since been replaced by industrial, financial capital, and urban real estate), its importance as measured by the capital/income ratio has remained steady and unchanged.

Thomas Piketty’s Second Fundamental Law of Capitalism

The third concept that Piketty spends time unpacking is what he calls his Second Fundamental Law of Capitalism. This law shows that countries with high savings rates and low growth rates accumulate enormous stocks of capital relative to their incomes over the long run. This can have significant effects on the social structure and distribution of wealth in a country. Piketty emphasizes that the impacts of this law are gradual and take decades to manifest. Boldly, Piketty predicts that by 2100 the entire planet could look like Europe at the turn of the 20th century with a capital/income ratio of 6-7 years.

The Dynamics of the Capital/Income Ratio in Europe and the U.S.

By investigating the dynamics of the capital/income ratio of Britain, France, Germany, and the United States, Piketty uncovers that the nature of capital in these rich countries has changed: capital was once mainly land but has now primarily become housing, industrial, and financial assets. But capital’s importance remains the same.

The Dynamics of the Capital/Income Ratio in Britain

In Britain, private wealth in 2010 accounted for 99% of national wealth and the bulk of the pubic debt in practice was owned by a minority of the population. Britain in summary is a country with accumulated capital based on public debt and the reinforcement of private capital.

The Dynamics of the Capital/Income Ratio in France

In France, private wealth in 2010 accounted for 95% of national wealth and the bulk of wealth in France was driven by accumulations of significant public assets in the industrial and financial sectors followed by major waves of privatization of these same assets. In a sense, France is a country with a model of Capitalism without Capitalists.

The Dynamics of the Capital/Income Ratio in Germany

In Germany, capitalism takes on a more social ownership point of view. Prevalent in the German marketplace is the stakeholder model of business where firms are owned not only by shareholders but also by certain other interested parties like the firms’ workers themselves. This Rhenish Capitalism has resulted in lower stock market valuations for German firms when compared to British & French firms.

The Dynamics of the Capital/Income Ratio in the United States

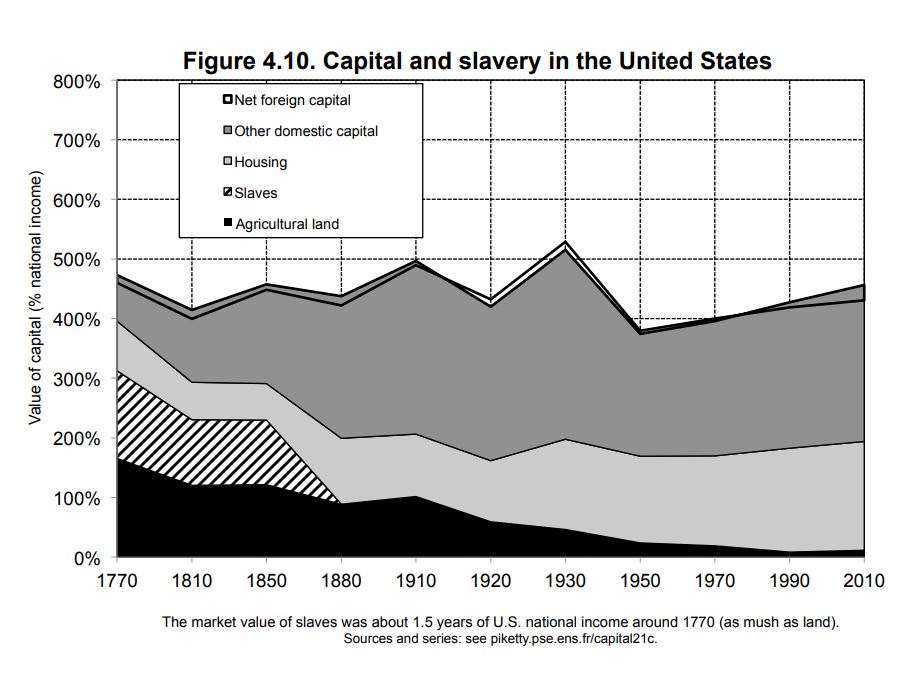

In the United States, more than 95% of the assets are American-owned but the influence of landlords and historically accumulated wealth was less important in the U.S. than in Europe. However, the structure of capital in the United States took on a different form. Specifically in the South, slave capital largely supplanted and surpassed landed capital. So much so, that the total market value of slaves represented nearly a year and a half of U.S. national income in the late 18th and first half of the 19th century.

Conclusion

A market economy based on private property, if left to itself, contains power forces of divergence, which are potentially threatening to democratic societies and to the values of social justice on which they are based. My next write-up on Capital in the Twenty-First Century by Thomas Piketty will dive into the immense inequalities of wealth that have occurred as a result of the natural dynamics of capital.