Introduction

What if I told you that the whole point of the stock market is not to make money? What if I told you that the stock market itself is just a Game, and the real object of this Game is not money; it’s the playing of the Game itself?

In The Money Game Adam Smith (also known as George J. W. Goodman) sets out to explain how the stock market is a Game to be played with objectives that oftentimes do not make sense. While money preoccupies so much of our consciousness, The Money Game is adamant that making money is not the real objective of playing the stock market Game. The sooner we realize that the stock market Game is an irrational one, the better we will play it.

Through a series of chapters asking questions and describing real events and real characters (real but masked), George J. W. Goodman sets out to explore the unexplored area of the markets … the emotional area. As he states very eloquently in Chapter 2, “There are fundamentals in the marketplace, but the unexplored area is the emotional area. All charts and breadth indicators and technical palaver are the statistician’s attempts to describe an emotional state.

In the end, the one requirement to win The Money Game is to remember the Irregular Rule: If you don’t know who you are, this is an expensive place to find out. Emotional maturity must be displayed over the long run if you are going to survive the game called the stock market.

My Summary Conclusions from Each Chapter

Part I. YOU: Identity, Anxiety, Money: Chapter 1-9

Preface: The game we create with it is an irrational one, and we play it better when we realize that, even as we try to bring rationality to it.

• Chapter 1: The word game was deliberately chosen to describe the stock market and the sooner that all of us small investors understand that this is a game, the better off we may be.

• Chapter 2: Do not forget the Irregular Rule: If you don’t know who you are, this is an expensive place to find out!

• Chapter 3: It all comes back to the Irregular Rule that you must know yourself for the stock market is an expensive place to find that out. The requirement to win this game is emotional maturity.

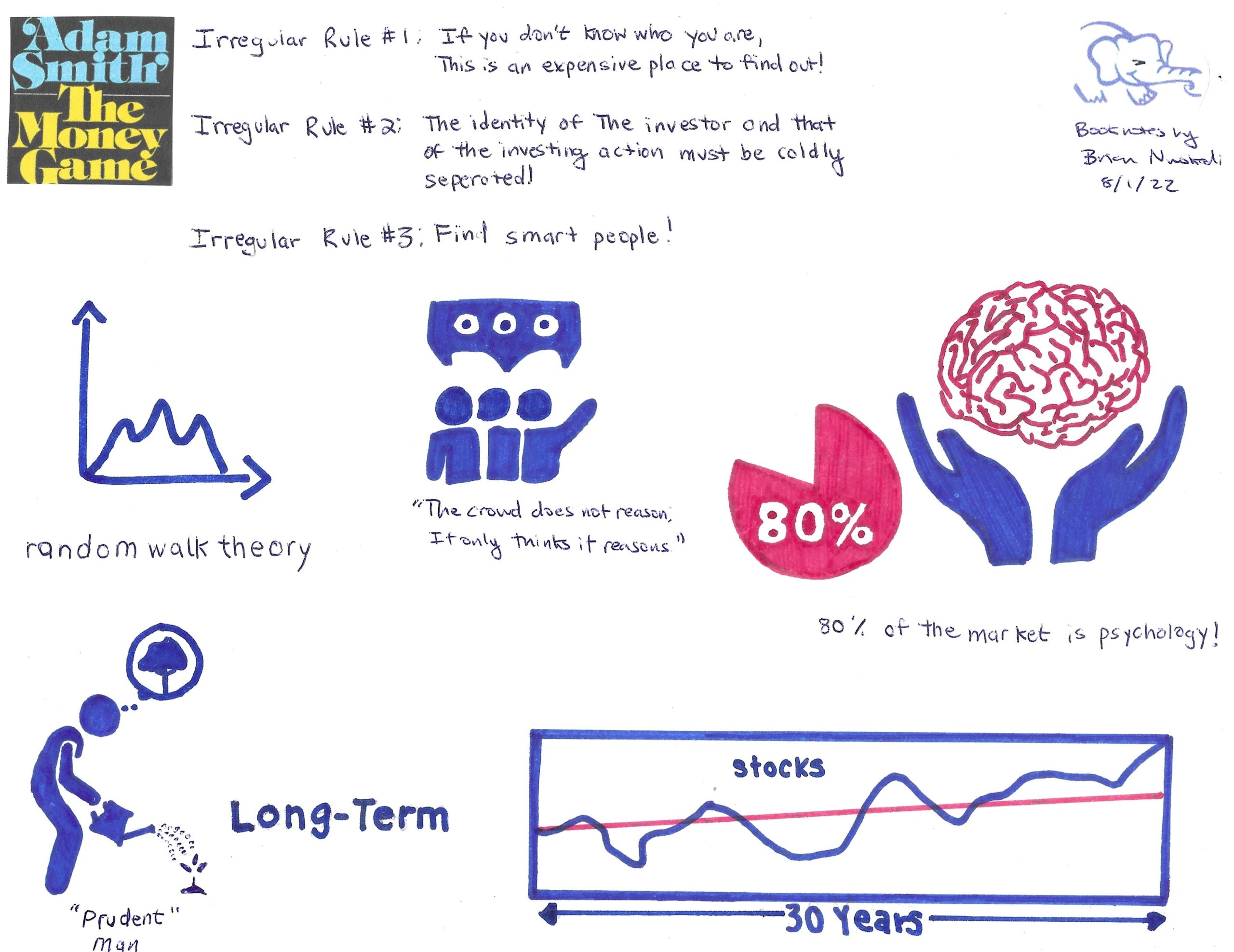

• Chapter 4: Since 80% of the market is psychology or deeper still human emotionality, the market can really be seen as a crowd. Because of this tendency, there is no substitute for good information, good research, and good ideas.

• Chapter 5: On one hand you have Adam Smith the father of modern economics stating definitely that money is about the maximization of profit and in some sense the accumulation of wealth (i,e. The Wealth of Nations). On the other hand, you have Norman Brown who sees money as a noose around our necks that ultimately makes our human nature impoverished. You must decide for yourself!

• Chapter 6: There are countless reasons people get into the Game. Some people love to gamble and lose. Others just want to make money over the long term by owning stocks forever. Regardless of your reason, you need to know yourself and stick to your plans.

• Chapter 7: The only real protection against all the ups and downs of the market (the anxiety) is to have an identity so firm it is not influenced by all the brouhaha in the marketplace. And remember, the stock doesn’t know you own it!

• Chapter 8: So if we are talking about real big money, forget the stock market. Build a company and have the market capitalize on your earnings.

• Chapter 9: The “simple equation of wealth”: To get rich, you find a stock whose _ has been compounding at a very fat, and then the stock zooms, and there you are.

Part II. IT: Systems: Chapter 10-14

Chapter 10: Charting assumes that what was true yesterday will also be true tomorrow. But you and I know that past patterns/performance are not predictive of future patterns/performance.

• Chapter 11: To quote Professor Fama, “the history of the series of stock price changes cannot be used to predict the future in any meaningful way. The future path of the price level of security is no more predictable than the path of a series of cumulated random numbers. If the random walk is indeed Truth, then all charts and most investment advice have the value of zero, and that is going to affect the rules of the Game.

• Chapter 12: The Game is such that computers take away any long-term advantages individuals find. Our only chance is to rely on luck (random walk thesis).

• Chapter 13: The numbers created by “independent auditors” should be looked at with a grain of salt given that the accountants are paid and hired by the companies themselves.

• Chapter 14: Someone has to be on the losing end of the transaction and that is usually the little investor.

Part III. THEY: The Pros: Chapter 15-18

Chapter 15: Professional investors are “performance” managers who are focused on driving results in the short term. Very few “performance” managers think in the long term. It’s all about driving big capital gains!

• Chapter 16: Like everything in life, those that are really in the know!

• Chapter 17: The market does not follow logic, it follows some mysterious tide of mass psychology.

• Chapter 18: If you are in the right thing at the wrong time, you may be right but have a long wait; at least you are better off than coming late to the party.

Part IV. VISIONS OF THE APOCALYPSE: Can it All Come Tumbling Down? Chapter 19-20

Chapter 19: Sooner or later you have to come to reality, and stop being a father to the world. Lead it, yes. Buy it. No.

• Chapter 20: Sure, it can all come tumbling down. All it takes is for belief to go away!

Part V. VISIONS OF THE MILLENNIUM: Do You Really Want to Be Rich?

Chapter 21: You need to create your own money philosophy to answer the question do you really want to be rich?

Visual Summary of Key Findings from Book

Downloadable Content – Raw Notes

Extras

Brian Nwokedi’s Book Review on Goodreads