Purpose of this article: to give you some tips to start building your credit history and explain why building up credit history is important to your financial well-being.

Overview

Credit is one of those tricky things … you need to have a solid credit history to get a decent credit card or a loan, but it’s hard to start building history when no one will give you credit in the first place. So what options do you have to establish credit history without credit in the first place? The following article will walk you through some solid options for building your credit history from scratch.

Option 1: Apply for credit card even with limited/no history

The best credit cards with the best interest rates are usually reserved for people with extended years of good credit history. If you are just starting out though, there are still a couple of credit card options for you even with limited or no credit history:

• Apply for a store credit card

Oftentimes stores extend credit cards to their customers with little to no credit history. These cards typically have very low credit limits and high interest rates, but they do give you a chance to prove that you can handle your finances in a responsible fashion. Once of my favorite store credit cards is the Target REDcard because it gives you 5% off every purchase every time and gives you free online shipping.

• Apply for an unsecured credit card (traditional credit card)

Traditional unsecured credit cards are not off the table when you have limited credit history. It just usually means that your credit card will have lower limits, more fees, and a higher interest rate associated with it. Credit card companies like to be compensated for taking on risk, and cardholders with limited to no histories bear the brunt of this. Credit Karma has a good list of unsecured credit cards for 2018.

• Apply for a secured credit card

If you are unsuccessful in opening a store credit card or a traditional unsecured credit card, your last credit card option is a secured credit card. With a secured credit card, you make a cash deposit upfront, say $300. This cash deposit serves as collateral against the credit card. You then charge the card accordingly and pay the card off each month. If you don’t make payments in full, you incur interest. The cash deposit is returned to you when you close the credit card. The key with secured credit cards is their duration of use should be short and only long enough to give you enough credit history to qualify for a better unsecured credit card. NerdWallet has a list of the best secured credit cards for 2018.

Option 2: Get a Co-signer or become an Authorized User

You have heard the adage that sharing is caring and with the co-signer or authorized user strategy, this adage really rings true. This is because when someone agrees to be your co-signer or allows you to be an authorized user on their credit card, they are ultimately committing to repaying your debts should you be unable to.

When someone agrees to be a co-signer to your loan they ultimately agree to pay off the loan if you cannot make the payments. When someone allows you to be an authorized user on their credit card they allow you to use their credit card and build history. But ultimately, they are legally obligated to pay for any charges unpaid.

Both situations require a huge degree of trust and should not be entertained lightly.

Option 3: Use your monthly rent to build credit history

Assuming you do not have a monthly mortgage payment (since you are just starting to build your credit history), you can use your on-time monthly rent payment to your landlord to build credit history.

Some landlords report positive payment history to the credit reporting agencies, and even if your landlord doesn’t, you can use a variety of rent-reporting services to get your positive payment history reported.

The only downfall of the rent-reporting services is that they aren’t free. I guess there is no such thing as a free lunch.

Option 4: Use your monthly student-loan payment to build credit history

The average student loan debt hover around $37,172 per person. If you happen to be one of the many citizens burdened with student loans, you can at least use your monthly on-time payments to build some positive credit history. This is because student loans are considered installment loans that are paid back over a set period of time.

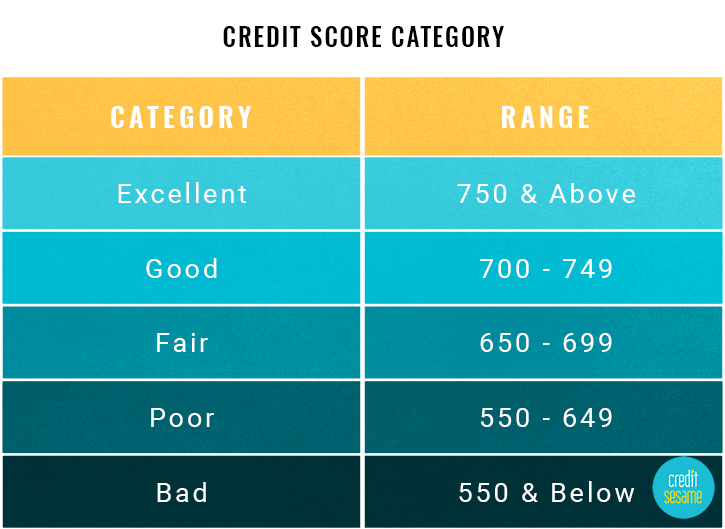

So, paying back your student loans on time will positively impact your credit history, and just staying on top of your loans each month is enough to boost your credit score into the 700+ range over time.

Closing

Your credit history good or bad can impact your ability to buy a home, purchase a car, get a better credit card, get cellphone coverage, and even impact the type of employment opportunities you may have.

Building and maintaining positive credit history takes some time. Remember that your credit history is really just a story that tells future lenders how you manage your financial affairs. If you are just starting out on your credit journey, you can use the strategies discussed above to navigate this process.

My hope in writing this article is that after reading this, you will take some steps towards successfully building your credit history.

{kind=link}