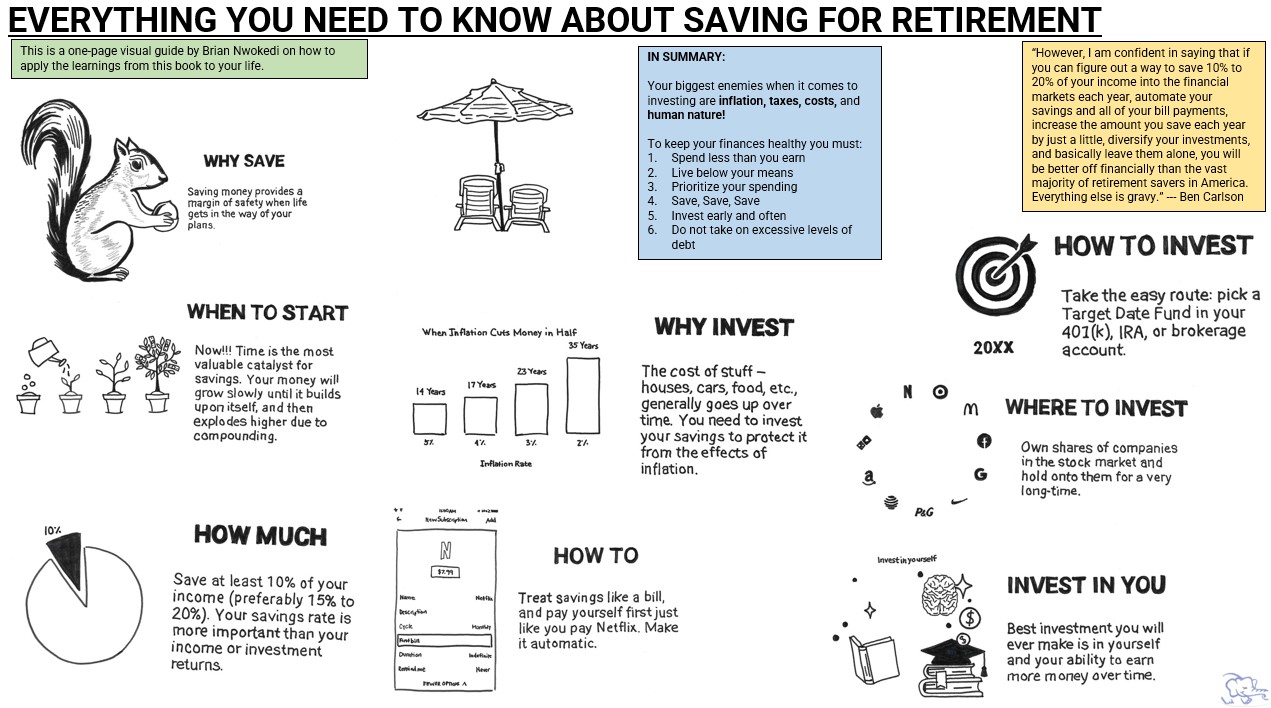

“However, I am confident in saying that if you can figure out a way to save 10% to 20% of your income into the financial markets each year, automate your savings and all of your bill payments, increase the amount you save each year by just a little, diversify your investments, and basically leave them alone, you will be better off financially than the vast majority of retirement savers in America. Everything else is gravy.” --- Ben Carlson(2020)

“Everything You Need to Know About Saving for Retirement“ by Ben Carlson is a succinct yet insightful guide that puts the spotlight on a fundamental aspect of retirement planning: your savings rate. In a world of complex investment strategies and ever-changing financial landscapes, Carlson distills his wisdom into a straightforward message – it’s not just about where you invest, but how much you save.

With a clear and approachable style, he emphasizes that building a secure retirement is within reach if you focus on increasing your savings and maintaining a consistent approach. Drawing on his expertise in personal finance, Carlson’s concise and no-nonsense approach empowers readers to take control of their financial destinies, offering a roadmap to achieving financial security during retirement through a smart savings strategy!

The following one-page visual guide has been created by me to help you apply the teachings from Ben’s book to your life. See below ?

Downloadable Content – Raw Notes

Ready to dive deeper into Ben Carlson’s work on Saving for Retirement? Download my unfiltered notes below ?

Purpose of this article: to define the emergency fund and help you put together a plan to increase yours.

Bullet Point Summary

Building an emergency fund to cover 3-12 months of expenses will take time

Focus first on saving $1,000 as soon as possible

Commit to saving all windfall payments you receive like tax refunds or any year-end company bonuses

Over the long-term you will need to spend less to save more and look to make more income overall

Building a good budget that helps you cut back on spending will be key

Save any yearly raise received. 1% to 3% can add up quickly

Rinse and repeat until you hit your goal

Overview

Ask any financial planner and they will tell you that an emergency fund is a must. Some will suggest you save upwards of three months of expenses while others will tell you one full year. In this article we discuss the ins and outs of the emergency fund and conclude by giving you strategies to boost your emergency funds.

What Are Emergency Funds For?

The ultimate point of the emergency fund is to set aside cash to cover your most basic needs during an unexpected life event. We all have differing wants and desires in life, but our basic biological requirements for survival are the same. When push comes to shove, we need air to breathe, food and drink, a place to lay our heads at night, and clothes to wear, as depicted in Maslow’s Hierarchy of Needs:

Maslow’s Hierarchy of Needs

Consequently, an emergency fund needs to be established to cover unexpected financial situations like the eviction from an apartment, loss of a job, medical bill, or temporary disability to name a few. In these situations, you’ll need immediate access to cash to cover your most basic expenses and needs while you get your financial situation back on track.

Is There a Right Number?

In a 2018 article, CNBC found that only 39% of Americans had enough savings to cover an $1,000 emergency. Defining the “right number” for an emergency fund is hard because financial emergencies by their very nature are unplanned and their lengths unknown. Instead, we suggest thinking through some of the larger types of unexpected life events that could cause you to dip into your emergency fund and planning specifically for those:

Loss of steady income from primary job – it takes roughly one month per $10,000 you make to find job per thebalancecareers.com. So a person making $50,000 a year would need at least five months of income saved up (roughly $21,000) to tidy themselves during their job hunt.

Car repairs and maintenance – depending on the severity of repair, costs can range from $300 for a water pump replacement up to $3,000 for a transmission replacement.

Major household repairs – similar to car repairs the cost of household repairs will very with the severity of the repair. An new HVAC system can cost 3,800+ while a new roof can run into the tens of thousands.

Using these four large unplanned expense, we build the following table to give you suggested savings targets at differing levels of income:

These savings targets are simply estimates and provide months of coverage ranging from 6 to 12 months. The most important thing is for you to see how expensive unplanned emergencies can be and start actively saving for them.

Short-Term Steps to Build Your Emergency Fund Over Time

It will take time to build a robust emergency fund with three to twelve months of expenses. With competing interests like saving for retirement and paying down debt, it can be difficult to find the extra cash needed to build your emergency fund. The following are the first couple of steps you can take in the short-term that will allow you to build temporary cushion for emergencies.

Your first step will be to save $1,000 as soon as possible. As we mentioned above, only 39% of Americans had enough savings to cover an $1,000 emergency. By focusing here, you are giving yourself a tangible goal that will help give you real cushion against any financial emergencies in the short-term. Set up an automatic transfer from your checking account to an online savings account like Ally of at least 3% of each paycheck. Someone making $40,000 would have over $1,000 in one year:

This assumes that your emergency fund doesn’t accrue any interest which isn’t the case especially if you put your funds in an Ally online savings account. As of the date of this article 5/22/19 Ally’s interest rate on their online savings account was 2.20%.

Your second step will be to save all windfall payments you receive like tax refunds or any year-end company bonuses you may receive. In the past tax refunds had averaged close to $2,100, but this year that was down to about $1,950. Even still, you should put this injection of cash directly into your emergency fund and get one step closer to peace of mind.

These steps are meant to help you build a temporary cushion for emergencies in a short amount of time. Once you complete these steps you will switch your focus to paying down debt if you are not debt-free. And once you are debt-free you will refocus on aggressively building a more robust and complete rainy day fund to cover three to twelve months of expenses.

Long-Term Steps to Build Your Emergency Fund Over Time

It will take time to build a robust emergency fund with three to twelve months of expenses. You should view view building enough emergency savings as a long-term project that will get easier as you free up more cash from the burden of life’s expenses.

Over the long run it will be important that you do two things very well: (1) spend less to save more and (2) make more income. As simple as this may seem, these two factors are the key to building your emergency fund in the long-run.

In order to spend less you will need to build a good budget that helps you cut back on spending. Knowing exactly how much you spend monthly will be key and we suggest using a digital app like Mint or You Need A Budget to track your expenses. The ultimate goal is to bring light to your monthly cash inflows and outflows which will help you free up funds to accelerate the growth in your cash reserves.

Boost your savings by bringing in more income through a side hustle or part-time job even if only temporarily. Make sure to save any yearly raises received. The average pay raise is around 3%, so a person making $40,000 would have an additional $1,200 to save towards the emergency fund over the next year.

Continue to execute the short-term and longer-term strategies discussed above until you hit your goal of three to twelve months of emergency savings.

Conclusion: Remember It Takes Time

An estimated 530,000 families go bankrupt each year because of medical issues, so it’s clear that medical expenses are a big unplanned life event. On top of unplanned medical expenses, there are a ton of other life events that happen unexpectedly that can derail your longer-term financial plans.

The only way to ensure that you will be truly financially secure in times of crisis is to build a robust and well-padded emergency fund. It takes some real time and effort to build a robust enough emergency fund that can handle three to twelve months of expenses, but it’s absolutely doable. We hope the strategies detailed within this article will give you a good enough guide to start building your emergency fund.

While it may be a hassle to create a financial plan, not knowing where you stand now makes it much harder to plan for where you need to be later in life, especially for retirement. At Blue Elephant Financial Services, we start our personal financial plan by taking a snapshot of your current Net Worth.

Your Net Worth is the sum of all of your Assets (i.e bank accounts, investments, car, home, etc.) minus your Liabilities or Outstanding Debts (i.e credit card debt, student loans, mortgage, car note, etc.)

The ultimate goal of the Blue Elephant Financial Services personal financial plan should be to drive towards increasing your Net Worth. The steps outlined below are my approach and strategy that will give you a sense of control, ultimately giving you the tools to drive towards financial stability:

1. Evaluate Your Spending Habits to see where we can trim expenses. The equation is relatively simple: Income – Expenses = Remainder. This remainder is positive when you spend less than you make. My job is to make you aware of how you spend your money, and work with you to cut out the “habitual & mindless” spending that ultimately hurts your long-term financial stability. Regardless of where your spending is, there is always an opportunity to trim and save/invest more.

2. Build an Emergency Savings Account that can sustain 3 to 6 months of expenses. While other financial planners will tell you to pay down your debt first, it is my belief that a lack of emergency funds leads to a perpetual cycle of more debt in the long-term, especially when emergency expenses arise. I always suggest that each of my clients save a minimum of $1,000 before turning their attention to paying off debt. This builds cash which increases your Net Worth. We make sure to automate this by contributing a minimum of $25.00 a month to an online savings account such as Ally. Set it then forget it. This simple step will trick your brain into feeling self-motivated.

3. Pay off all High Interest Credit Card Debt. Any outstanding debt that is above 10% needs to be a primary focus of your financial plan. Paying off your credit will (+) increase your Net Worth, ultimately freeing up more of your funds to do other things with. Once you pay off your credit card debt, you will no longer be held back by principal, interest payments, and finance charges. This then frees up more of your funds to build your emergency savings and/or invest in your retirement account, which leads to better long-term growth in your Net Worth. On an aside, utilization rate of your credit card should never go above 30%.

4. If applicable, you should Pay of Any Outstanding car notes, student loans, and other non-mortgage debts with interest rates below 10%. Once you have eliminated your high interest credit card debt, you will now have a decision to make. I always suggest that extra funds should go towards paying off outstanding non-mortgage debt. The sooner you can get out of debt, the better off your future returns will be, ultimately driving significant gains in your Net Worth.

5. Once you have eliminated mindless spending, built an emergency fund, paid off high interest debt, and eliminated other outstanding non-mortgage debt, you are ready to Rapidly Ramp Up Your Retirement Savings. Your goal should be to save enough money so that you can live at 50% -70% of your current income. If your employer has a matching 401 (k), you should contribute enough from day one to get the match. Keep your investment allocation simple by picking a blended index fund as your retirement vehicle.

Blue Elephant is here to tailor your financial plan to meet your needs. Our plans always focus our efforts on maximizing your Net Worth which helps you ultimately meet your current and ongoing financial obligations.