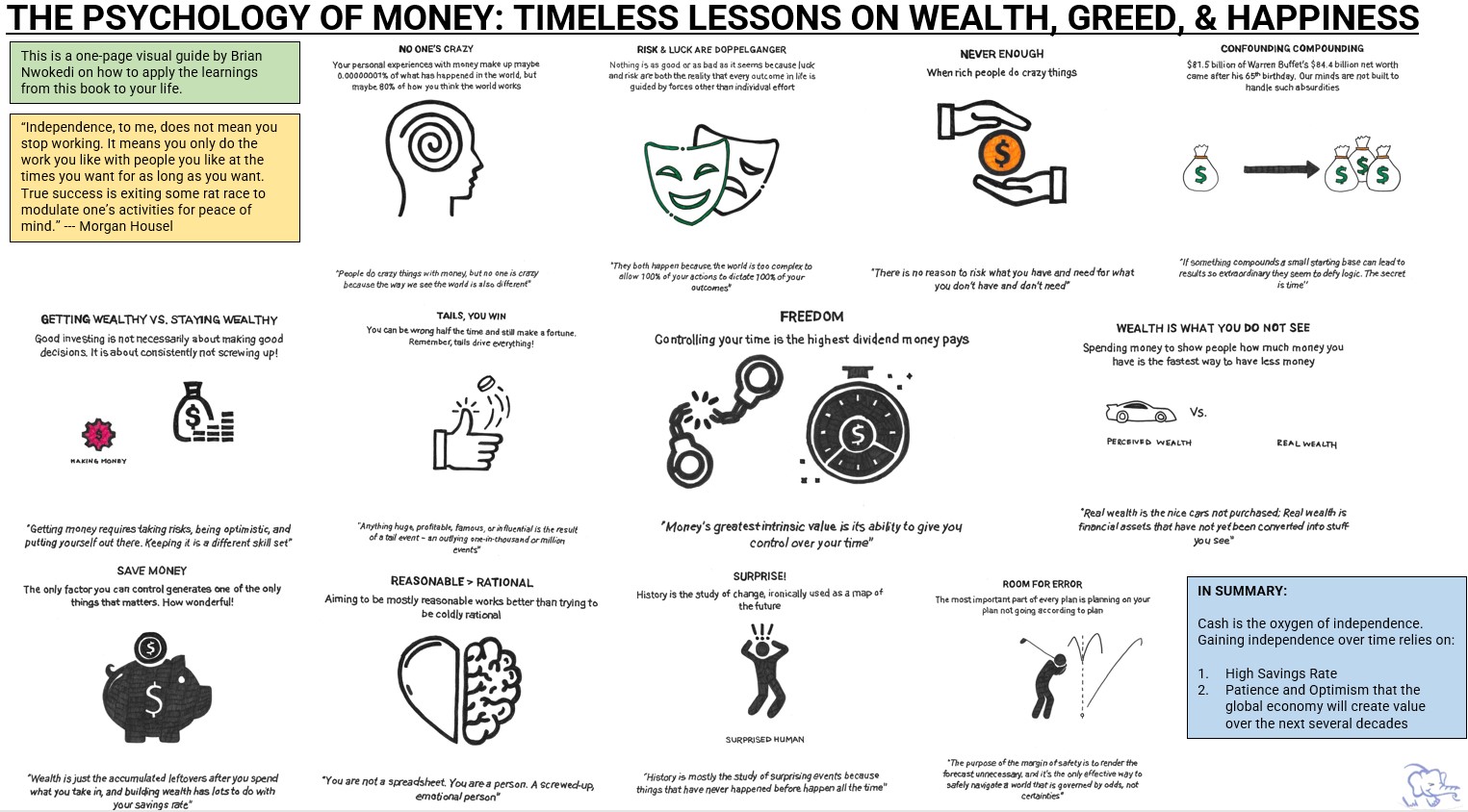

"Success with money relies more on Psychology than Finance,and doing well with money has little to do with how smart you are, and a lot to do with how you behave. And behavior is hard to teach, even to really smart people." --- Morgan Housel (2020)

“The Psychology of Money“ by Morgan Housel is an insightful guide that puts the spotlight of financial success squarely on the shoulders of human behavior. In this world of complexity, how you behave with money is more important than what you know about money.

With a blend of research, anecdotes, and stories of personal experiences, Housel illuminates the significance of better understanding your own behavior, and how that is far more responsible for your financial outcomes than your skill.

The following one-page visual guide has been created by me to help you apply the teachings from Morgan’s book to your life. See below ?

Downloadable Content – Raw Notes

Ready to dive deeper into Morgan Housel’s work on The Psychology of Money? Download my unfiltered notes below ?

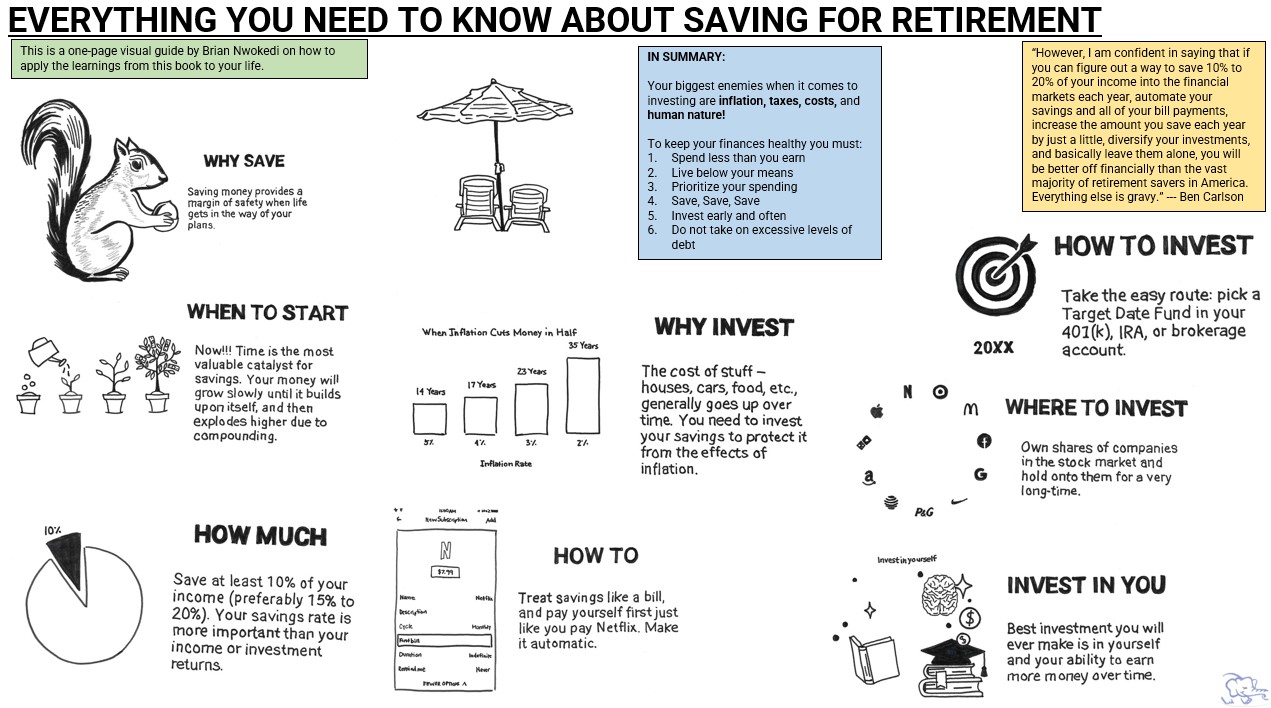

“However, I am confident in saying that if you can figure out a way to save 10% to 20% of your income into the financial markets each year, automate your savings and all of your bill payments, increase the amount you save each year by just a little, diversify your investments, and basically leave them alone, you will be better off financially than the vast majority of retirement savers in America. Everything else is gravy.” --- Ben Carlson(2020)

“Everything You Need to Know About Saving for Retirement“ by Ben Carlson is a succinct yet insightful guide that puts the spotlight on a fundamental aspect of retirement planning: your savings rate. In a world of complex investment strategies and ever-changing financial landscapes, Carlson distills his wisdom into a straightforward message – it’s not just about where you invest, but how much you save.

With a clear and approachable style, he emphasizes that building a secure retirement is within reach if you focus on increasing your savings and maintaining a consistent approach. Drawing on his expertise in personal finance, Carlson’s concise and no-nonsense approach empowers readers to take control of their financial destinies, offering a roadmap to achieving financial security during retirement through a smart savings strategy!

The following one-page visual guide has been created by me to help you apply the teachings from Ben’s book to your life. See below ?

Downloadable Content – Raw Notes

Ready to dive deeper into Ben Carlson’s work on Saving for Retirement? Download my unfiltered notes below ?

What if I told you that the whole point of the stock market is not to make money? What if I told you that the stock market itself is just a Game, and the real object of this Game is not money; it’s the playing of the Game itself?

In The Money Game Adam Smith (also known as George J. W. Goodman) sets out to explain how the stock market is a Game to be played with objectives that oftentimes do not make sense. While money preoccupies so much of our consciousness, The Money Game is adamant that making money is not the real objective of playing the stock market Game. The sooner we realize that the stock market Game is an irrational one, the better we will play it.

Through a series of chapters asking questions and describing real events and real characters (real but masked), George J. W. Goodman sets out to explore the unexplored area of the markets … the emotional area. As he states very eloquently in Chapter 2, “There are fundamentals in the marketplace, but the unexplored area is the emotional area. All charts and breadth indicators and technical palaver are the statistician’s attempts to describe an emotional state.

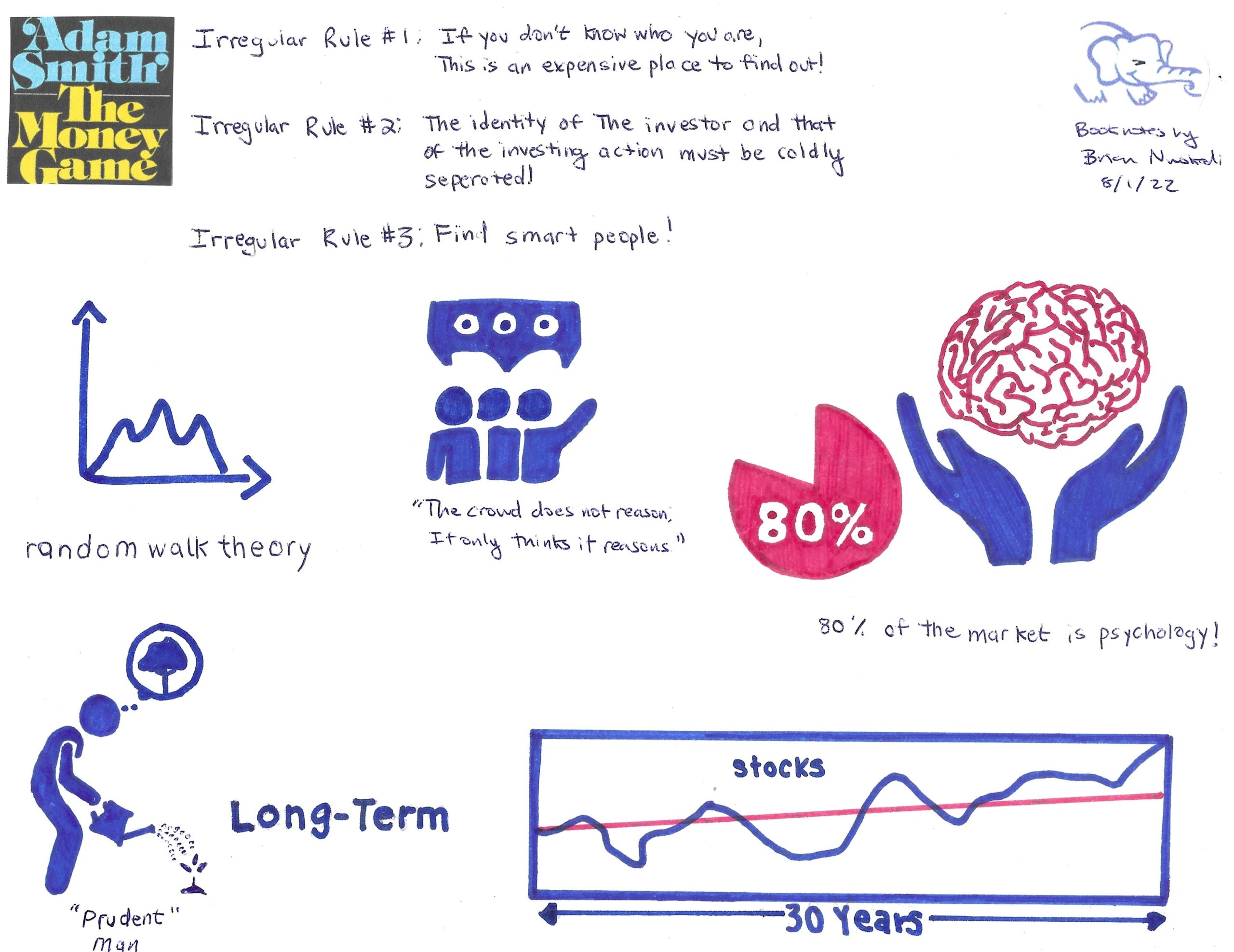

In the end, the one requirement to win The Money Game is to remember the Irregular Rule: If you don’t know who you are, this is an expensive place to find out. Emotional maturity must be displayed over the long run if you are going to survive the game called the stock market.

My Summary Conclusions from Each Chapter

Part I. YOU: Identity, Anxiety, Money: Chapter 1-9

Preface: The game we create with it is an irrational one, and we play it better when we realize that, even as we try to bring rationality to it.

• Chapter 1: The word game was deliberately chosen to describe the stock market and the sooner that all of us small investors understand that this is a game, the better off we may be.

• Chapter 2: Do not forget the Irregular Rule: If you don’t know who you are, this is an expensive place to find out!

• Chapter 3: It all comes back to the Irregular Rule that you must know yourself for the stock market is an expensive place to find that out. The requirement to win this game is emotional maturity.

• Chapter 4: Since 80% of the market is psychology or deeper still human emotionality, the market can really be seen as a crowd. Because of this tendency, there is no substitute for good information, good research, and good ideas.

• Chapter 5: On one hand you have Adam Smith the father of modern economics stating definitely that money is about the maximization of profit and in some sense the accumulation of wealth (i,e. The Wealth of Nations). On the other hand, you have Norman Brown who sees money as a noose around our necks that ultimately makes our human nature impoverished. You must decide for yourself!

• Chapter 6: There are countless reasons people get into the Game. Some people love to gamble and lose. Others just want to make money over the long term by owning stocks forever. Regardless of your reason, you need to know yourself and stick to your plans.

• Chapter 7: The only real protection against all the ups and downs of the market (the anxiety) is to have an identity so firm it is not influenced by all the brouhaha in the marketplace. And remember, the stock doesn’t know you own it!

• Chapter 8: So if we are talking about real big money, forget the stock market. Build a company and have the market capitalize on your earnings.

• Chapter 9: The “simple equation of wealth”: To get rich, you find a stock whose _ has been compounding at a very fat, and then the stock zooms, and there you are.

Part II. IT: Systems: Chapter 10-14

Chapter 10: Charting assumes that what was true yesterday will also be true tomorrow. But you and I know that past patterns/performance are not predictive of future patterns/performance.

• Chapter 11: To quote Professor Fama, “the history of the series of stock price changes cannot be used to predict the future in any meaningful way. The future path of the price level of security is no more predictable than the path of a series of cumulated random numbers. If the random walk is indeed Truth, then all charts and most investment advice have the value of zero, and that is going to affect the rules of the Game.

• Chapter 12: The Game is such that computers take away any long-term advantages individuals find. Our only chance is to rely on luck (random walk thesis).

• Chapter 13: The numbers created by “independent auditors” should be looked at with a grain of salt given that the accountants are paid and hired by the companies themselves.

• Chapter 14: Someone has to be on the losing end of the transaction and that is usually the little investor.

Part III. THEY: The Pros: Chapter 15-18

Chapter 15: Professional investors are “performance” managers who are focused on driving results in the short term. Very few “performance” managers think in the long term. It’s all about driving big capital gains!

• Chapter 16: Like everything in life, those that are really in the know!

• Chapter 17: The market does not follow logic, it follows some mysterious tide of mass psychology.

• Chapter 18: If you are in the right thing at the wrong time, you may be right but have a long wait; at least you are better off than coming late to the party.

Part IV. VISIONS OF THE APOCALYPSE: Can it All Come Tumbling Down? Chapter 19-20

Chapter 19: Sooner or later you have to come to reality, and stop being a father to the world. Lead it, yes. Buy it. No.

• Chapter 20: Sure, it can all come tumbling down. All it takes is for belief to go away!

Part V. VISIONS OF THE MILLENNIUM: Do You Really Want to Be Rich?

Chapter 21: You need to create your own money philosophy to answer the question do you really want to be rich?

Visual Summary of Key Findings from Book

“Unfortunately, as we have seen, the playing of the Game is not entirely a rational affair. There is nothing so disastrous, said Lord Keynes as a rational investment policy in an irrational world”

Purpose of this article: to share a contrarian investment approach with consistent results that speak for themselves.

Bullet Point Summary

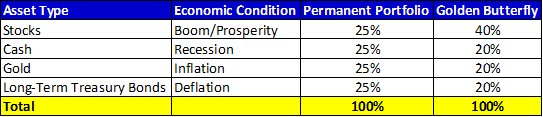

The Golden Butterfly Portfolio is built as an extension of the Permanent Portfolio

The Permanent Portfolio selects assets that perform in four distinct economic realities:

Choose stocksto capture returns during economic Prosperity

Choose cash & short-term treasuries to capture returns during economic Recession

Choose gold to capture returns during periods of economic Inflation

Chooselong-term treasuriesto capture returns during periods of economic Deflation

The Golden Butterfly Portfolio is more aggressive than the Permanent Portfolio with a higher allocation placed in stocks.

This portfolio protects you and grows your money regardless of what happens in the general global economy and it may be perfect for the “set it and forget it” investor.

Overview

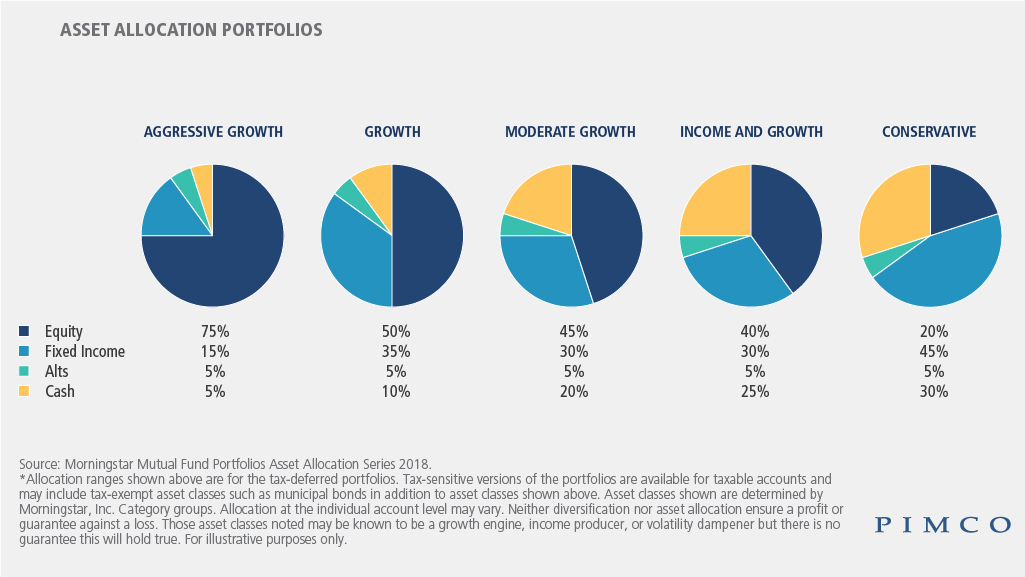

Whether you are a seasoned investor or new to investing, choosing the way you divide your investment up can be a daunting task. Google the word “asset allocation” and you will get over 164 million results. As shown in the following graphic from PIMCO Investment Management, there are five traditional methods to allocate your investments across different assets:

Building the right portfolio to capture long-term returns can feel like an endless exercise in futility. Some of us go at this alone, while others of us leverage money managers and investment advisors. Regardless of the approach, we all hope to end up with enough investment returns to retire comfortably. My hope with this article is to offer you a new and simple asset allocation that helps you set your investments and forget them until retirement.

What Is The Golden Butterfly Portfolio?

In 1998, Harry Browne wrote Fail-Safe Investing where he spelled out his principles for the “Permanent Portfolio.” The underlying thesis to his approach was that four economic conditions have historically occurred at varying frequencies throughout the years. By allocating investments in equal weights across stocks, bonds, cash, and gold, Browne theorized that his Permanent Portfolio would perform well regardless of the changing economic conditions.

The Golden Butterfly is essentially a more aggressive version of Browne’s Permanent Portfolio. Under the Golden Butterfly Portfolio, the exposure to stocks is increased from 25% to 40% while the exposure to Treasury bonds, cash, and gold are reduced from 25% to 20% respectively. The following chart details the differences between the Permanent Portfolio and the Golden Butterfly Portfolio:

By allocating your investments this way, you can take a more neutral outlook on a given economic condition. This investment approach grows your money no matter way the future holds.

How Does The Golden Butterfly Portfolio Stack Up Over Time?

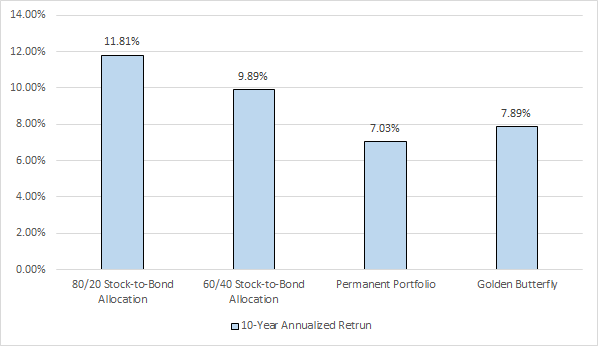

The following performance comparison is through September 30, 2020:

As you can see from the above, the clear winner has been the 80/20 stock-to-bond allocation which returned +11.81% over the last 10 years. But it is important to note that over the past 10 years, the economic conditions have been categorically Boom/Prosperity and the stock market has been on an unprecedented run. Thus portfolios with more exposure to stocks have done better over the past 10 years, than portfolios with less exposure to stocks.

Both the 80/20 stock-to-bond allocation and the 60/40 stock-to-bond allocations have more stock exposure than the Permanent Portfolio (only has 25% stock exposure) and the Golden Butterfly Portfolio (only has 40% stock exposure). And as such, they have performed better overall than both of those portfolios. It’s important to note though that investing in stocks carries more risk than investing in bonds or gold.

By investing in the Golden Butterfly Portfolio, you are giving yourself a chance to grow your money as seen in the +7.89% over the past 10 years. And you are doing so in a less risky fashion since only 40% of your portfolio is exposed to stocks. The downside though is in Boom/Prosperity economic conditions, the Golden Butterfly Portfolio underperforms other portfolios with more stock exposure as shown in the graph above.

What is Right for You?

As I mentioned in the beginning of this write up building the right portfolio to capture long-term returns can feel like an endless exercise in futility. But only if you lose site of what you are trying to accomplish. Investors that are interested in setting a portfolio that grows their money while mitigating overall risk will be very interested in the Golden Butterfly portfolio.

While this portfolio sacrifices a lot of the upside of other more aggressive portfolios, it’s simplicity for the average investor or beginning investor outweighs this fact. You should heavily consider investing in the Golden Butterfly Portfolio if you are looking for an asset allocation that is simple and effective at growing your money over the long-term while allowing you to not worry about specific economic conditions.

The Extras…

Here is video on how exactly you can build the Golden Butterfly using index funds.

Purpose of this article: to convince you that a switch to passive investing will boost your chances of hitting your long-term investing and wealth generating goals

Bullet Point Summary

Since 1926 the entire gain in the U.S. stock market is attributable to just 4% of stocks.

Well over 40% of stocks generated 0% return since 1989 and underperformed even Treasury Bills.

To top this off, the top 86 stocks have created 50% of the total $32 trillion generated in the stock market from 1926 to 2015.

These improbable sounding stats point to a mathematical principle called Positive Skew, which ensures that only a handful of active investors will pick and own the right stocks that turn into big winners.

The Positive Skew of stock market returns ensures there will always be more losers than winners.

Consequently, switching to passive investing and indexing is the only tangible and consistent solution to combating the dynamic of Positive Skew.

Overview

I consider myself an educated investor that at best can generate okay to modest returns on average. Even though I take the time to evaluate individual stocks, invest in companies at “the right” price point, and hold for the long-term, I can’t consistently generate over-the-top returns in my active portfolio. And neither can many of my smart counterparts on Wall Street with their enormous informational and financial resources.

Inherently I have always known that trying to beat the market is a fool’s errand. And while books like Fooled by Randomness and A Random Walk Down Wall Street remind me of the difficulties of consistently besting the market, it was an article on Bloomberg I recently read that put the nail in the coffin of active investing for me.

The thesis of the article is very simple:

Not only can’t humans outdo benchmarks, we can’t even fight them to a draw.

Why Do We Suck So Hard at Consistently Picking Winners?

While it is important for active investors to do their homework when it comes to compiling an investment strategy the actual reality of the stock market is that all this effort is futile. When push comes to shove the fundamental reason why active investing sucks so hard is that the distribution of returns in the stock market is bizarrely lopsided.

Because of the statistical principle of Positive Skew (see picture below), only a handful of active investors will pick and own the right stocks that turn into big winners. The rest of the market simply will not.

By Rodolfo Hermans (Godot) at en.wikipedia. – Own work; transferred from en.wikipedia by Rodolfo Hermans (Godot)., CC BY-SA 3.0, https://commons.wikimedia.org/w/index.php?curid=4567445

The Positive Skew of stock market returns means that there will always be more losers on the left side of the distribution than winners who end up on the right side of the distribution with better than average returns.

History Clearly Shows Stock Picking Losses for Most Active Investors

The math and statistics are simply not in your favor if you are an active investor. The nature of the stock market is such that the odds are stacked against active investors when it comes to consistentlypicking winners. On average, there will be a small number of extreme winners, a small number of extreme losers, and a ton of stocks that will oscillate around average performance. As a result, most everyone outside of an indexer owns mostly deadbeat stocks.

The following chart from A Wealth of Common Sense shows exactly this as well over 40% of stocks generated 0% return since 1989 and underperformed even Treasury Bills.

And in 2017, Hendrik Bessembinder found that since 1926 the entire gain in the U.S. stock market is attributable to just 4% of stocks. And to top this off, he also found that the top 86 stocks created 50% of the total $32 trillion generated in the stock market from 1926 to 2015.

Just stop for a second and let that all sink in… And once you have, call your active money manager and request a change in strategy.

Conclusion: Switch to Passive Investing

For most of us, switching to passive investing and indexing is the only tangible and consistent solution to combating the dynamic of Positive Skew. With active investing comes a much greater chance of underperformance that inherently comes when you attempt to pick stocks. And consequently, active investors need to realize that the statistical disadvantage of Positive Skew is an uphill battle that most of them will lose.

It’s simply impossible to actually know which companies will be the outsized winners (think about trying to place a bet on Amazon and Google circa 1998). The only real option is a diversified passive investment strategy which spreads your investment dollars across a lot of different companies. This simplistic and effective approach is best positioned to beat the statistical dynamic of Positive Skew in the stock market.